Can $10B Manipal Hospitals Become the Apollo of This Generation?

Pharmacy

Last fortnight, Manipal Health Enterprises filed its Draft Red Herring Prospectus with SEBI for an Rs. 8,000 crore IPO. The largest healthcare listing India has ever seen.

Before the First Bed

In 1953, Tonse Madhava Ananth Pai looked at a stretch of barren red laterite rock on the Karnataka coast and decided it was the right place to build a medical college.

There was nothing there. Just the outskirts of Udupi and the particular stubbornness of a man who had spent years watching independent India fail to train enough doctors for its own people. The government had a plan for this, as it had plans for most things, but it was not working fast enough. TMA Pai, physician, banker, and educationist, had decided that waiting was a strategy for getting old.

In 1953, he opened Kasturba Medical College on that barren hill. The first private, self-financing medical college in India. The establishment thought this was eccentric. Then, characteristically, he did not stop.

In 1957, Manipal Institute of Technology came up on the same red rock. A dental college followed, then pharmacy, then pre-university. Each one built on the same stubborn model: private funding, no government support, every rupee of surplus reinvested back into the institution. Since the campus kept growing but had nowhere to house the thousands of students and faculty it was attracting, he built the town too, roads, housing, canteens, post offices, until the hill that had been empty a decade earlier had the shape of a small city.

His philosophy was a clean loop. Charge fair fees, reinvest the surplus, and the institution improves, attracting more students, generating more surplus. The entire thing was designed to run without donor dependency or government patronage. If this sounds familiar, it is because every VC in the country would call it a bootstrapped model with great unit economics.

TMA Pai had also co-founded Syndicate Bank, so he understood how capital moved across time, and how institutions needed a kind of patience that governments and donors rarely possessed. By the mid-1970s, tens of thousands of students had passed through what the family would eventually call MEMG, or the Manipal Education and Medical Group. Many of them were now practising doctors and engineers scattered across India and abroad.

He was also watching what was happening to India's public hospitals. The government network was buckling, a population growing faster than the infrastructure meant to serve it. A family that had spent two decades producing those doctors was quietly beginning to wonder whether just producing them was enough.

The hospitals were not yet part of the picture. But the question was forming.

The University Ward

TMA Pai died in 1979. He left behind a university town built from nothing and institutions that could stand on their own. His son, Ramdas Pai, inherited the group. The loose federation of colleges consolidated into Manipal Academy of Higher Education, later recognised by the UGC as an Institute of Eminence, among the highest formal recognitions an Indian university can receive.

Four years after TMA Pai's death, something happened in Chennai that the Pais noticed.

In 1983, Dr Prathap Reddy opened Apollo Hospitals. He was a cardiologist who had trained in the US and returned to India convinced that the country was ready for a different kind of hospital - private, world-class, unafraid to charge. Most people told him he was wrong. He opened anyway

Apollo's opening was not just a business event. It was a proof of concept. Private healthcare in India could work, and someone had proved it.

The irony was not lost on the Pais. Every doctor Apollo needed had been trained somewhere. Kasturba Medical College had been producing those doctors for thirty years. The family had, without intending to, been building the human infrastructure that made Apollo's bet viable and was now watching someone else collect on it.

Manipal Hospitals opened its first facility in Bangalore in 1991. Not as a commercial venture, but as a teaching hospital, an extension of the education mission, a place where Kasturba faculty could see patients while training the generation after them. The logic was identical to Apollo's: build something serious, fill a gap that the government cannot.

What followed was supposed to be straightforward, but theory is cheaper than practice.

Decade on the Drip

The Pai family had spent four decades training India's doctors. In 1991, they opened a hospital for those doctors to practise in. It lost money from the first year.

Not catastrophically or all at once. But consistently. Revenue was not being tracked the way it needed to be. Beds sat unoccupied when they should not have. Procedures were priced without understanding their true cost. The supply chain was managed loosely. All the discipline that TMA Pai had applied to building his education empire had somehow not transferred to the hospital.

The fundamental problem was cultural, and it ran deep. A hospital run by doctors, for doctors, optimises for clinical outcomes. Survival rates, research output and peer recognition. These are not bad priorities. But they are not sufficient, on their own, to keep a large institution financially viable.

Nobody was asking the hard business questions. How much does it cost to admit each patient? What is the bed occupancy rate, and why is it not higher? Which procedures actually generate margin, and which ones are losing money? What does the patient experience from arrival to discharge actually look like?

The losses were not dramatic enough to force an immediate decision. The hospital had patients, it had a reputation tied to the Manipal name, and the broader group was profitable enough to absorb the shortfall. Manipal Technologies, the group's print and digital services business, was growing steadily. The academic arm was stable and respected. The hospital situation persisted. Year after year, the hospital generated goodwill but not enough income.

The institution the family had built on a philosophy of financial self-sufficiency, in its newest venture, depended on the rest of the group to survive.

Meanwhile, Apollo was compounding.

Through the 1990s, Dr Prathap Reddy was building exactly the kind of business discipline the Pai family's hospital was missing. Apollo was tracking revenue per bed, investing in technology, building a referral network, and marketing itself to international patients. It was becoming a brand. The gap between what Apollo was building and what Manipal was not building was widening every year.

Then Ranjan Pai arrived.

Ranjan was the grandson of TMA Pai. He had grown up watching his family manage large, complex institutions and absorbed, almost by osmosis, the business logic beneath the academic surface. In the early 2000s, he stepped into the healthcare business and moved fast.

His diagnosis was direct. The hospital was not being run like a business because no one with actual business experience was running it. The fix was not subtle. Bring in professional managers, give them real authority, and move the retired professors back to what they were genuinely excellent at.

Professional managers took over hospital administration, revenue management, supply chain, and operations. For the first time, the hospital started being run with the same discipline that TMA Pai had applied to his educational institutions. Beds were tracked. Revenue was measured. Patient experience was taken seriously.

The cultural shift did not happen overnight. But the direction was unmistakably different by 2003. Revenue was starting to improve. Losses were beginning to narrow. The question now was whether this was a recovery or the beginning of something much larger.

The Doctor Takes Charge

By 2003, the hospital that had bled money for a decade was starting, slowly, to breathe on its own.

The Bangalore flagship, under the new discipline, became something the industry took notice of. It was rated the best hospital in the city for 11 consecutive years. The clinical quality had always been there. What changed was everything around it.

India’s larger healthcare story was also moving in a direction that made the timing matter.

The burden of chronic disease was rising. Public infrastructure was still stretched. And the middle class, growing faster than ever, was becoming more willing to pay for something better and more reliable.

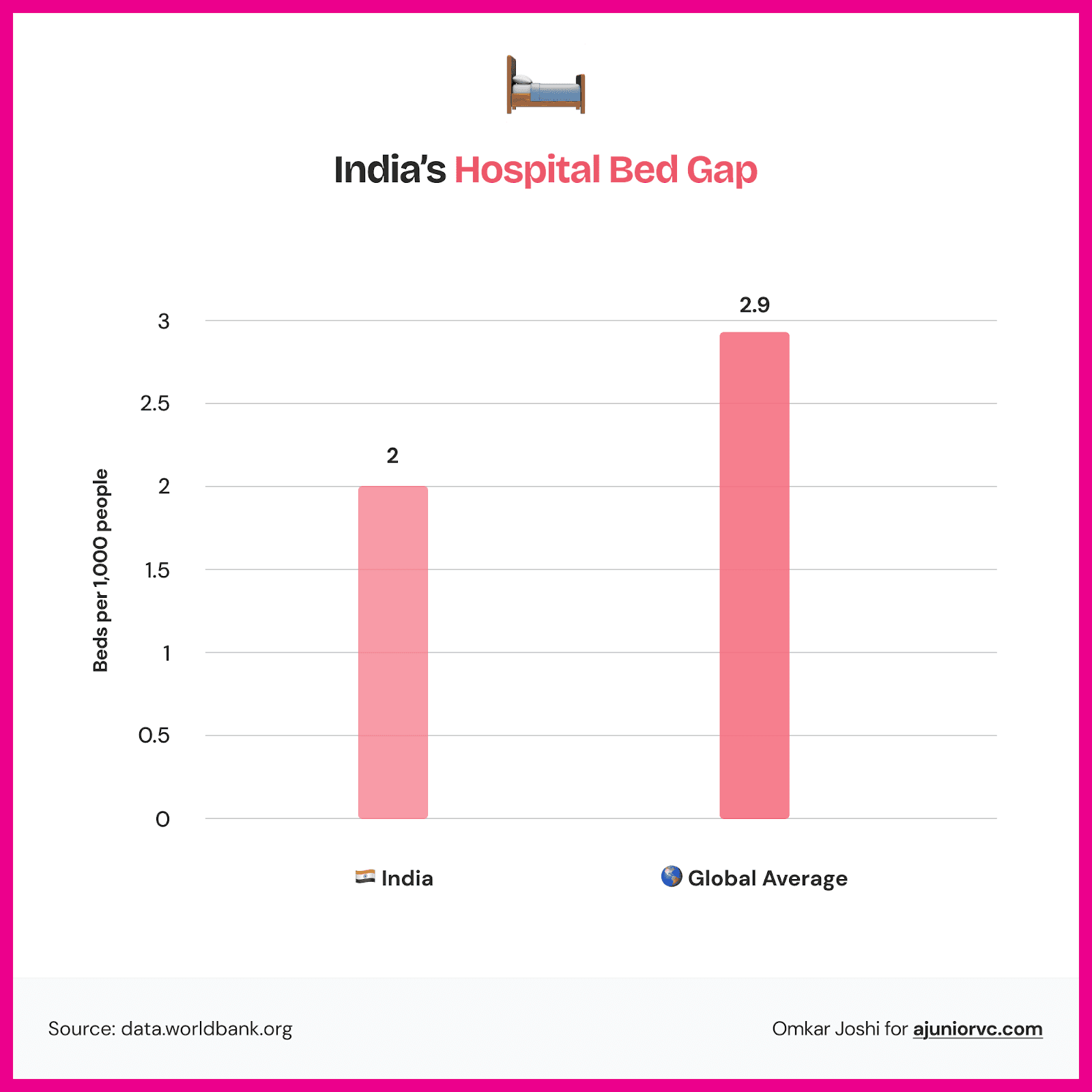

Even the numbers showed how wide the gap still was. In 2003, India had just 2 hospital beds per 1,000 people, while the global average was close to 3. Even by 2010, that gap had not closed meaningfully.

What the country needed and what it actually had were still very far apart. That gap was not going to disappear quickly. It was a structural deficit that would take years to close.

Which is what made the insurance shift so important.

Health insurance penetration was still low, around 25% of the population, but it was moving. Private insurers were growing. Employers were beginning to offer health cover as a standard benefit. The shift from out-of-pocket to insured healthcare was beginning to make private hospitals a more predictable business.

That did not solve the capacity problem. But it changed the economics around it. Private hospitals became a little more predictable as a business because demand was no longer coming only from households making one difficult payment at a time.

Institutional investors were paying attention.

In November 2010, Kotak Private Equity made the first significant external investment in Manipal Hospitals through a Series A round. By that point, Ranjan Pai had been running the turnaround for nearly a decade. The Bangalore flagship's record spoke for itself. Kotak was not taking a leap of faith. It was investing in a proven operator in a sector that would only become more important.

The chain had grown to roughly ten hospitals, all in South India, all producing improving numbers. Apollo had taken three decades to become a national name. The question Manipal was now beginning to ask was whether there was a faster way.

They needed to just look around

First, Do No Harm

By the early 2010s, India's private hospital sector had produced four very different kinds of empires.

Each one was a bet on a different theory of what patients wanted and what a hospital business could become.

Apollo was the godfather. By 2012, it had been running for nearly thirty years, had over 50 hospitals across India, and had built a brand so trusted that patients would travel across the country to reach it. It had pioneered medical tourism in India, attracting patients from the Gulf and Southeast Asia who came specifically for complex cardiac and oncology care. The Apollo model was simple: go premium, go complex, and make your hospitals so capable that distance is no longer a reason not to come.

Max had drawn the opposite conclusion. Rather than trying to be everywhere, Max concentrated all of its energy in Delhi-NCR and became the dominant name in that market through sheer operational focus. Max proved that owning a city beats owning a map.

Fortis was the cautionary tale the sector studied quietly. The Singh brothers had built a national chain through aggressive acquisitions. By the early 2010s, they were one of the largest private hospital groups in the country, but the governance cracks were beginning to show, the promoter controversies were surfacing, and the story of what happens when ambition outruns discipline was being written in real time.

And then there was Narayana Hrudayalaya, which we had written of in great detail. Dr Devi Shetty, once Mother Teresa's personal physician, had decided that the entire pricing model for cardiac care in India was wrong. His answer was volume: do the procedure ten thousand times, drive the cost per case down to a fraction of what anyone else was charging, and prove that affordable does not mean unviable. By the early 2010s, Narayana was already treating more cardiac patients than almost any other hospital group in the world.

Four chains, four completely different answers to the same question. And Manipal, sitting in South India with 15 hospitals and a spotless clinical reputation, fitting neatly into none of them.

It had the clinical reputation of Apollo without Apollo's three decades of brand equity. The operational focus of Max without Max's geographic lock-in. It had not made Fortis's governance mistakes. And it was not chasing Narayana's volume model. It was the best hospital chain that not enough people outside South India had heard of. That was the problem, and the opportunity.

Apollo had taken thirty years to build its moat. Manipal was looking at that timeline and doing the arithmetic. Thirty years was not available. The sector was filling up fast. It needed a different approach entirely. Every serious investor in Indian healthcare had been watching the same four empires take shape. Then they looked south.

In December 2011, Manipal Hospital Bangalore became the first hospital in India to receive AAHRPP accreditation, the internationally recognised gold standard for ethical clinical research, and the sixth in all of Asia. That was not a marketing exercise. It was a signal to the global medical community that this institution operated to the same standards as the world's best research hospitals.

In November 2012, True North and Faering Capital backed Manipal in a Series B round. True North had a track record in Indian healthcare and brought more than a cheque. It brought the institutional credibility that signalled to the next tier of investors that this was a serious business being run seriously.

Then came February 2015. TPG Capital took a 22% stake in Manipal Health Enterprises for Rs. 900 crore. Premji Invest and IDFC Private Equity came in alongside. TPG's thesis was direct: India's middle class was growing, insurance coverage was expanding, and the disease burden was not going anywhere. Private hospitals were not a luxury business. They were infrastructure. Manipal, with its clinical reputation and a turnaround story now fifteen years deep, was exactly the platform to build on.

By 2015, Manipal had roughly $1 billion in cumulative backing from Kotak, True North, Faering Capital, TPG, Premji Invest, and IDFC. Fifteen hospitals. A balance sheet that could finally support something much bigger. The investors were ready, but the network was not.

Operating on Opportunity

In 2018, Fortis Healthcare came up for sale.

The Singh brothers' governance crisis had finally caught up with the company. When it hit the market, the entire sector showed up to bid. Manipal entered, backed by TPG, with a credible offer and a clear integration plan. The combination would have created India's largest hospital chain by revenue, with 41 hospitals and over 11,000 beds. The Fortis board engaged. Then everything went sideways. Competing bids from IHH Healthcare and the Hero-Burman consortium, months of shareholder opposition, and multiple revised offers. It became one of the messiest corporate auctions in Indian healthcare. In the end, Manipal walked away.

That missed a fire.

Ranjan Pai had just watched a chain of 34 hospitals go to someone else. Manipal had the capital, the management, and the track record. What it lacked was enough of its own scale to be the obvious buyer in a room full of serious bidders. He decided to fix that permanently.

In 2019, Manipal Group moved in an entirely different direction. It acquired TTK Group's 31.48% stake in Cigna TTK Health Insurance, a joint venture between Cigna Corporation and TTK that had been in place since 2014. The company was renamed ManipalCigna. For the first time, the group was on both sides of the healthcare equation: delivering care through its hospitals and covering its costs through insurance. The same patient, from the same family, using the same brand at every point in their healthcare journey.

The opportunity to build scale arrived with COVID.

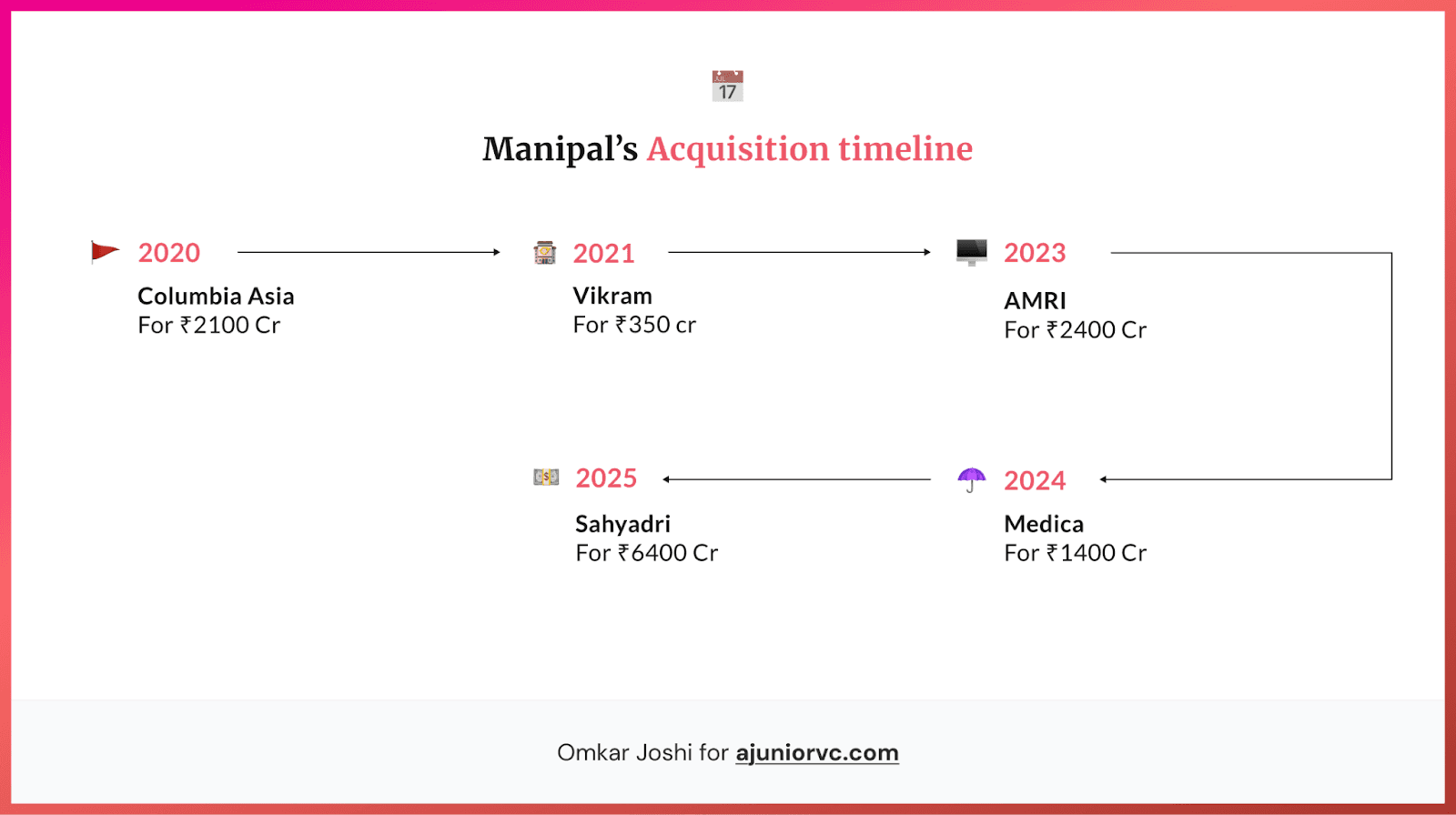

In 2020, Columbia Asia, a Malaysian hospital network with eleven well-run, operationally tight facilities spread across Bengaluru, Pune, Mysore, and other cities, needed to exit India. Manipal paid Rs. 2,100 crore. In one transaction: 1,600 new beds, five new cities, and a network built to international standards. While the rest of the sector was managing the pandemic, Manipal was buying the infrastructure to outlast it.

That kind of conviction, deployed in that kind of moment, attracted a different kind of capital. In April 2021, NIIF - the National Investment and Infrastructure Fund, the Indian government's own vehicle for long-horizon institutional money, put Rs. 2,100 crore into Manipal Health Enterprises. NIIF does not back startups. It backs bridges, ports and power grids. Its arrival was a quiet but unmistakable signal: private hospital capacity in India had shifted from an investment thesis to something closer to national infrastructure.

The Acquisition Ward

Before the land grab that followed, there is one number worth keeping in mind.

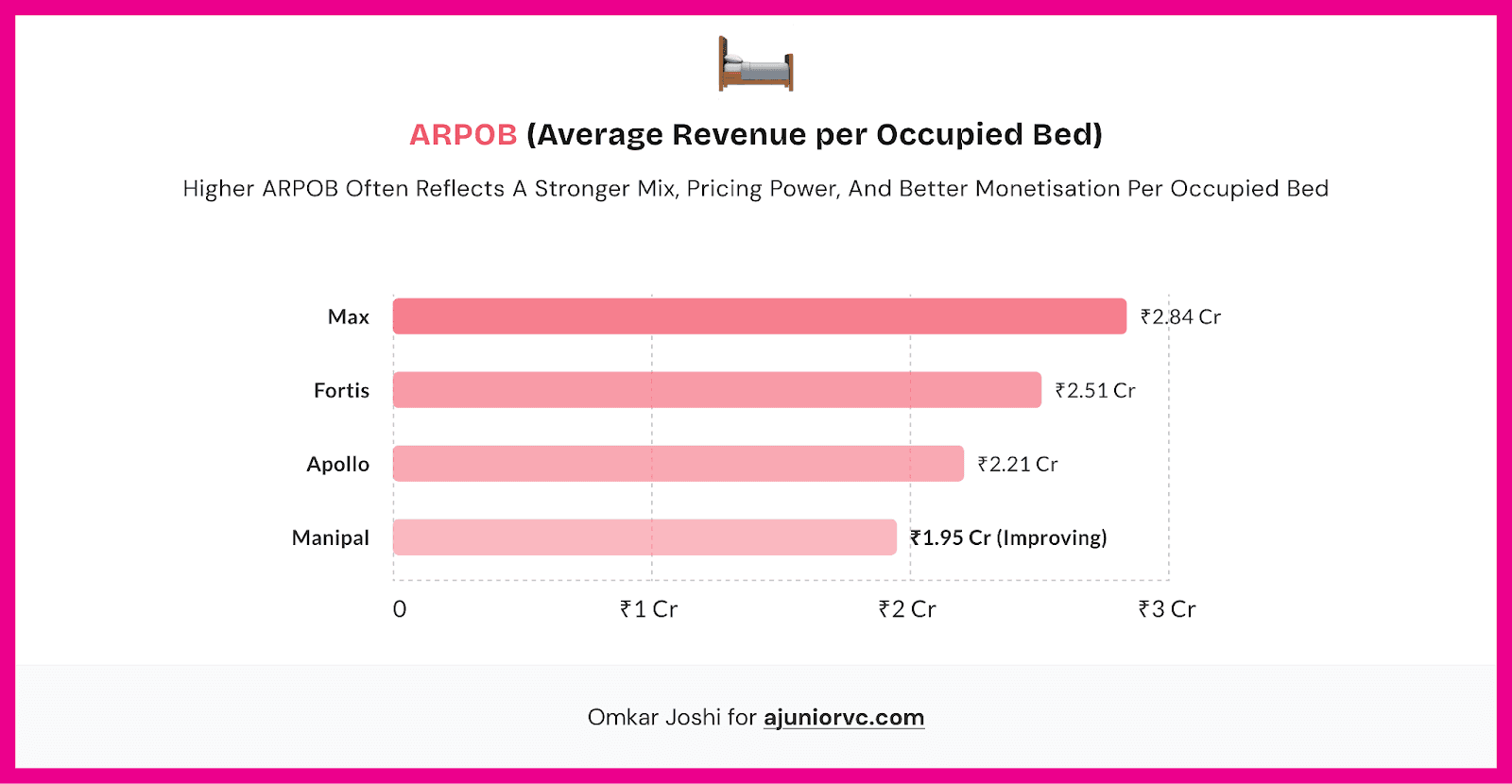

ARPOB - Annual Revenue Per Occupied Bed - is the measure that separates hospitals that are merely large from hospitals that are genuinely efficient. Max leads the sector at Rs. 2.84 crore per occupied bed per year. Fortis follows at Rs. 2.51 crore. Apollo at Rs. 2.21 crore. Manipal trails all three. It would soon have more beds than any other hospital in India. It was not yet extracting as much from each one. That gap is the operating problem the next five years have to solve, and it matters because every acquisition that follows makes sense only if the beds being bought can eventually perform.

The same month as the NIIF deal, Vikram Hospital in Bengaluru was acquired for Rs. 350 crore. The chain crossed 25 hospitals.

Every serious hospital chain in India had a Kolkata story. Manipal did not - until it acquired an 84% stake in AMRI Hospitals for Rs. 2,400 crore. Six hospitals, over 2,000 beds, and a foothold in a city that had been conspicuously absent from every South India-anchored chain's geography. Eastern India was underpenetrated and largely unserved by organised private healthcare. Manipal was looking at it the same way TMA Pai had once looked at a barren hill in Udupi.

The AMRI deal brought the biggest endorsement yet. In 2023, Temasek - Singapore's sovereign wealth fund - acquired a 41% stake from NIIF for approximately Rs. 16,300 crore, bringing its total holding to 59% and valuing the entire company at around $5 billion. For a hospital that had spent the 1990s quietly bleeding money, that was not a small number.

In February 2024, a Series E round brought in $85 million from Mubadala, Abu Dhabi's sovereign wealth fund, alongside Novo Holdings - the investment arm of the Novo Nordisk Foundation - and CalPERS, the California Public Employees' Retirement System. Sovereign capital from Singapore, Abu Dhabi, Denmark, and a US pension fund, all backing the same Indian hospital chain.

In April 2024, Manipal acquired an 87% stake in Medica Synergie for Rs. 1,400 crore - another eastern India operator, more beds in West Bengal, a second anchor to go alongside AMRI. The eastern India bet was no longer a bet.

Then came the biggest deal yet. In July 2025, Manipal acquired Sahyadri Hospitals from Ontario Teachers' Pension Plan, Maharashtra's largest private hospital network, with 11 facilities across Pune, Nashik, Ahilya Nagar, and Karad. Rs. 6,400 crore. Maharashtra, India's single largest consumer economy, was inside the network. The same year, KKR provided $600 million in structured debt financing to the broader Manipal Group, its largest private credit deployment in India to date.

The numbers at the end of FY25 told the story.

Revenue had gone from Rs. 4,839 crore in FY23 to Rs. 8,242 crore ~ a 70% jump in two years. Net profit from Rs. 414 crore to Rs. 1,081 crore, a 161% increase. In terms of revenue, Manipal had already overtaken both Max Healthcare and Fortis Healthcare. 49 hospitals, 12,000 beds, 14 states, five years. Over Rs. 12,000 crore in acquisitions across seven separate deals.

But beneath those numbers, a tension was accumulating. 7 acquisitions in five years meant seven different hospital cultures that had not yet been reconciled into one. AMRI had its own clinical habits built over decades in Kolkata. Sahyadri had been shaped by a Canadian pension fund with its own operating philosophy. Columbia Asia had been run by a Malaysian parent to international standards that differed from Manipal's. A patient walking into a Manipal hospital in Pune and a patient walking into one in Kolkata were not, in any meaningful sense, having the same experience yet. The supply chain was not unified. The clinical protocols were not unified. The referral networks ran in parallel rather than together.

Manipal had bought the beds, but had not yet built the hospital.

On March 24, 2026, Manipal filed its DRHP with SEBI. An Rs. 8,000 crore fresh issue, an offer for sale from existing investors, and a potential pre-IPO placement of Rs. 1,600 crore - a total raise north of $1 billion. The lead managers: Kotak, Goldman Sachs, JP Morgan, Jefferies, Axis Capital, UBS, and DBS.

Of the fresh issue, Rs. 5,378 crore goes toward clearing debt. Another Rs. 574 crore to mop up the remaining minority stake in Sahyadri. Manipal is not coming to the public markets to fund the next acquisition, but to pay off the last five.

Manipal built the hospitals, but the IPO is paying for the beds.

The Long-Term Prognosis / Scale Is Not Yet System

Can Manipal Hospitals become the Apollo of its own generation?

Apollo became what it is by being first. Dr Prathap Reddy opened in 1983 when the idea of a private hospital chain in India was genuinely radical. He had four decades to build brand recognition, clinical depth, and the kind of trust that makes patients travel six hundred kilometres rather than go to the nearest hospital. By FY25, Apollo was doing Rs. 21,794 crore in revenue across 73 hospitals, with a market cap above Rs. 1 lakh crore. Its ARPOB stood at Rs. 2.21 crore per year. That is what forty years of compounding looks like.

The tailwinds that made Apollo possible have only strengthened. India's hospital market is expected to grow from $122 billion today to $202 billion by 2030. Health insurance penetration has gone from 25% of the population in 2013 to 65% in 2023. India's total health expenditure nearly doubled in four years. The money is flowing into the sector. The question is only who has the network to capture it, and Manipal, by beds and by cities, has made sure the answer cannot easily exclude them.

The cap table says the world has already made its bet. At listing, the market cap is expected to land meaningfully above the $5 billion mark from 2023. Apollo trades above Rs. 1 lakh crore today, or $10 billion. That gap is the entire pitch to every analyst who opens the DRHP.

Apollo became Apollo because it had time. Manipal is trying to compress forty years into ten. It has the capital, the footprint, and the momentum. What it does not yet have is a single unified system - the kind that makes a patient in Pune and a patient in Kolkata feel that they are inside the same institution.

It is also worth remembering what Manipal actually is. The hospital chain is one division of a much larger family story. MEMG also runs Manipal Academy of Higher Education (an Institute of Eminence), UNext (an online education platform), and ManipalCigna Health Insurance. The IPO is a liquidity event for one arm of a conglomerate that TMA Pai began on a barren hill in 1953, which, depending on how you look at it, is either a footnote or the whole point.