Has India’s $60B Didi Economy Finally Found Its Startup Moment?

Profile

Weddings

Last fortnight, Snabbit reported 830,000 orders in February 2026 alone, while Pronto scaled from 1,000 to 18,000 daily bookings in just seven months, pushing its valuation past $100M within a year of launch.

Gold Rush

In 2012, Debadutta Upadhyaya was a working mother in Mumbai with an infant at home and no support system.

She launched Timesaverz after running into a problem millions of urban Indian women already knew well. Finding reliable help with the home was still an exhausting, referral-driven process.

As she was figuring out how to build, Ola happened too.

Not to Timesaverz specifically. To every investor in the country simultaneously. Ola had shown that one of India’s most chaotic informal sectors could be made predictable through software. You pressed a button, a driver showed up, payment happened digitally, ratings built trust, and a messy offline market looked platform-ready.

The inference was immediate. If you could dispatch a cab predictably, you could dispatch anything.

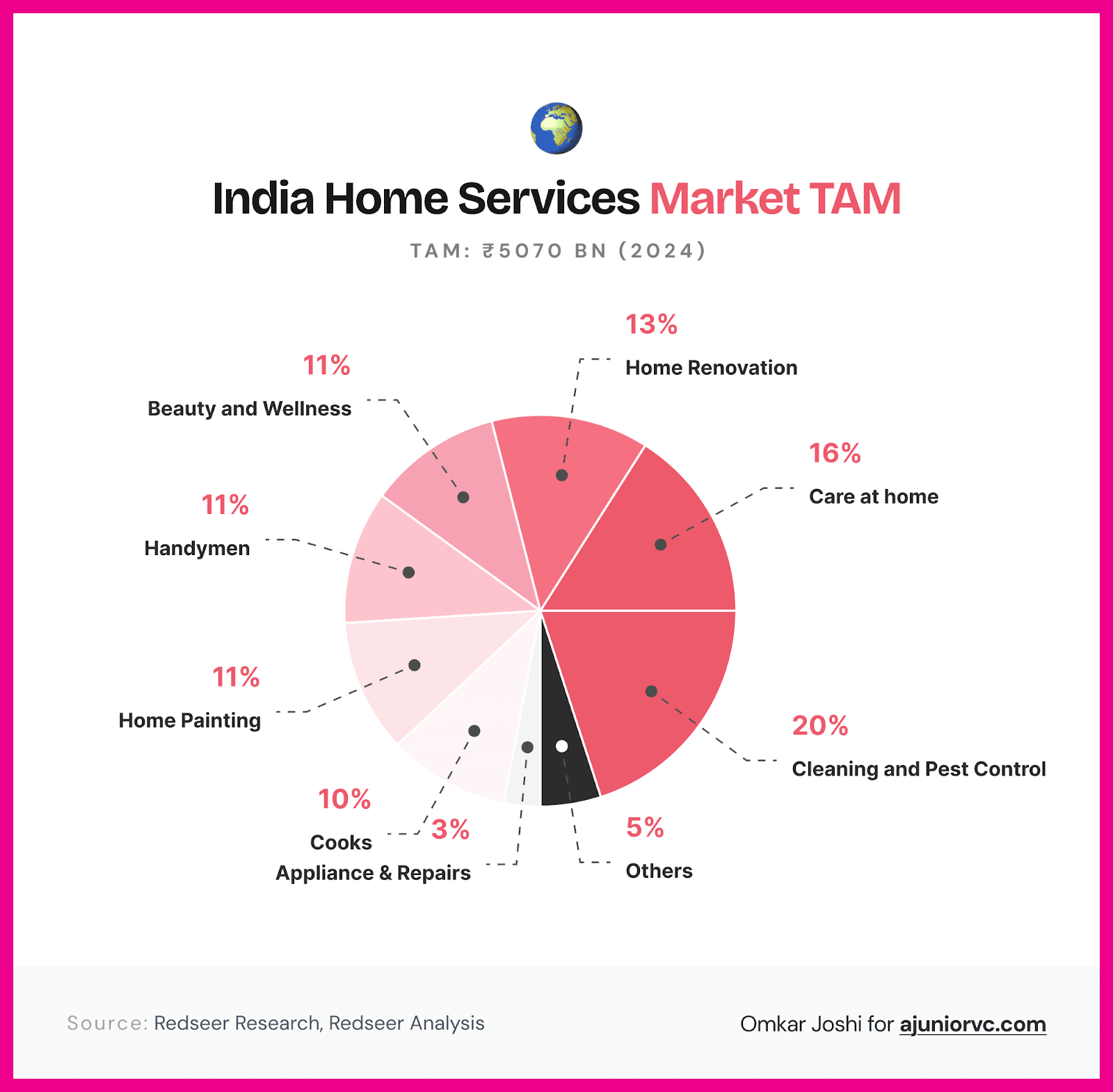

Home services looked like the most obvious target of all. Fragmented supply. Smartphone penetration was rising fast. A TAM that analysts were putting at ₹3 to 5 lakh crore, with essentially zero digital penetration. The spreadsheet looked beautiful.

Service ticket: ₹500-₹800. Worker payout of ₹350 to ₹500. The platform charges a rate of 20-30%. This left roughly ₹100 to ₹200 per order with no inventory, warehouses or owned labour force. On Excel math, it was a large, under-digitised, multi-lakh-crore market with existing demand and existing supply, and a clean margin structure in between.

The gold rush began.

Within 18 months, a cluster of startups arrived with almost identical ambitions - UrbanClap, Housejoy, Zimmber, LocalOye, Taskbob, Doormint, EasyFix, and yes, Timesaverz, which had been there before all of them. There would be an astonishing 69 home services startups founded in 2014 alone. Didis, electricians, plumbers, and carpenters were all going to be at your doorstep instantly. In a single year.

It looked like a giant, homogenous category being won. It wasn’t.

The ecosystem had bundled episodic household services and daily domestic infrastructure into one market and applied the same marketplace logic to both.

But they behaved like completely different systems.

An electrician showed up when something broke. A didi shows up every morning because the home does not run without her.

Debadutta had started with the right instinct: the daily friction of the home, the working mother, the nuclear family with no support system. The market that followed her went somewhere else entirely.

In the shining light of home services, lay the unheralded corner of the Didi Economy.

Don’t Fix What Ain’t Broken

India did not need help discovering domestic labour. It had already built one of the largest household workforces in the country long before anyone thought to put it on an app.

India already had roughly 4.5-5 crore domestic workers. That is a staggering number. For context, India’s IT sector employs around 54 lakh people. Even the gig economy was estimated at roughly 1-1.5 crore workers. Domestic work was not some hidden corner of the labour market. It was already one of the biggest labour systems in urban India.

It was not economically broken either.

A typical worker did not depend on one home. She stitched together work across 4 to 6 households, often earning ₹2,000 to ₹4,000 per home every month. That could mean a monthly income of roughly ₹15,000 to ₹25,000, built not through a single employer but through a small portfolio of homes. On the other side of the transaction, the household was effectively paying just ₹80 to ₹120 per visit for something that was not occasional convenience, but part of the daily functioning of the home.

That is what made this system so powerful. It was informal but not inefficient.

Long before platforms spoke about supply aggregation, Indian neighbourhoods had already figured out how to distribute. The watchman knew who had just left a nearby flat. A neighbour passed along her cook's number before the cook moved out. One employer referred a cleaner to three more homes in the building.

Entire migration chains connected villages and districts in Bihar, Jharkhand, Uttar Pradesh, and Odisha to the demands of Delhi, Mumbai, Bengaluru, and other cities. Labour moved through trust, familiarity and repetition, not software.

That was the real challenge underneath the category.

Any platform trying to build here was not entering a broken market waiting to be fixed. It was entering a market that already worked - cheaply, locally and at scale. By 2015, more than a $100M had been plowed into the home services category.

But a storm was coming.

Crashing Wave

By 2016, the romance of the first-wave startups had begun to wear off.

The problem was not demand. Indian homes clearly needed plumbers, electricians, AC technicians, carpenters and cleaners. The problem was that these businesses were never as clean as they looked in the first deck.

A repair booking is messy the moment real life enters it.

A leaking pipe is not the same as a broken washing machine. An AC that is “not cooling properly” on the phone can turn into a gas refill, a spare parts issue, or a half-day service call once the technician gets there. A carpenter's job that sounds minor can eat up hours. One visit solves the issue. The second becomes a callback. The third becomes a refund. The final one becomes a customer-support argument about who is actually at fault.

The platform was not just matching labour. It was stepping into chaos, and the math started breaking exactly there.

A typical booking might be around ₹600. The platform would keep roughly ₹150, but acquiring that customer could itself cost ₹350. Then came the rest of the damage - support costs, failed bookings, refunds, rework, and the general operational mess of trying to standardise services that were not naturally standard. Another ₹75 could disappear there very quickly. The economics were weak even before one thing made it worse: frequency.

Most repair and maintenance services were not habits.

A household may book them once a year, maybe twice if something goes wrong. That meant CAC could not be recovered through lifetime value. Startups were spending heavily to acquire transactions that had no natural repeat curve. They were not building compounding customer relationships. They were often just buying one-off demand and hoping the math would improve later.

For a while, funding covered that illusion. Then, it didn’t

Between 2016 and 2017, the category started filling up with cautionary tales. Taskbob shut down. Doormint shut down. EasyFix got acquired. Zimmber got acquired by Quikr. LocalOye went through layoffs and restructuring. Housejoy kept surviving, but only by reshaping itself again and again. What looked in 2014 like a giant breakout market was, just a few years later, beginning to look like a graveyard of startups that had mistaken a large category for a scalable one.

Through the mayhem, one startup managed to evade the sucker punch to the grave.

Survival of the Slimmest

Urban Clap stayed alive because it understood early what it needed to do to survive.

It did not survive because the original model was sound. It survived because it moved away from that model faster and more decisively than everyone else.

The early wave had largely behaved like lead-generation marketplaces. Find demand, pass the job to supply, and keep a cut. That was fine as long as the platform remained a thin layer. But a thin layer cannot control outcomes, and in home services, outcomes are the whole business. Urban Clap started pulling more of the service inside the company’s control.

It trained workers, used standardised tools and tightened pricing. UC reduced category sprawl. It stopped treating every local service as equal and focused much more on the ones where quality could actually be made predictable.

It stopped trying to organise everything and started choosing what could actually be organised. That is why beauty became so important.

A salon-at-home service behaved much better than repair and maintenance. It was easier to define, easier to train for, easier to quality-check and, most importantly, much more frequent. A good customer could come back 8 to 10 times a year. Ticket sizes could be ₹1,500–₹2,000. At that point, a 20–30% commission starts to look like a business, not a hope. Repeat gave UC something the rest of the category never really had: the ability to recover CAC over time and still leave room for a contribution margin.

That is what the first wave had missed.

A big market is not enough, and even massive demand is not enough. The category must behave in a way that allows the platform to recoup the costs of acquiring and controlling the customer.

By 2018, UC found a way to survive by moving toward categories with predictable outcomes, tighter control and real repeat. While sharpening its focus, the labour market that ran the everyday Indian home, daily sweeping, utensils, cooking, childcare, eldercare, still sat outside this model. That work was too continuous, too trust-led, and too woven into the household routine to be treated as a managed service slot. The first wave of startups barely bothered to scratch its surface, and as UC slimmed it wasn’t going to try this battl.e

The first wave had gone after “home services” as one giant market. What survived was a much narrower truth.

Changing Homes

By 2019, it wasn’t just startups trying to change this market. The Indian home itself was changing.

A decade earlier, domestic work in urban India was embedded in a broader social structure. Families were larger. Parents or in-laws were often around. Neighbours knew each other for years. The watchman knew which worker came to which flat. The aunty downstairs usually had a number. Discovery did not feel like a market problem because trust was already moving before the worker entered the home.

By 2019, that scaffolding had thinned.

Homes had become more nuclear. More couples were living away from family, and more households were being run without the older support systems that once absorbed the daily friction of the home. Female labour force participation, which had risen to 25% in 2018 overall and much higher urban areas, changes more than in labour markets outside the home. It changes the house itself. The time once available to find help, manage help, replace help, or absorb the chaos when help doesn’t show up starts shrinking.

Urban India was changing in another way, too.

The country was filling up with new apartment towers, gated societies and residential clusters where people had square footage, but not social memory. In older neighbourhoods, a house often came with a local referral chain built in. In newer ones, the flat was ready before the trust network was. A family moving into a tower in Bengaluru, Gurugram, Pune, or Hyderabad might have the need, the urgency and the money, but not the local map of who to call.

The money had begun to matter much more.

India’s average annual gross household income had risen from ₹3.9 lakh in 2010 to ₹5.2 lakh in 2019, and the number of affluent households earning ₹10–20 lakh a year had doubled from 1.3 Cr to 2.6 Cr. This was not just a story about rising incomes. It was a story about a different willingness to pay for reliability, for speed, and for not having to solve the same household problem through referrals every single time.

That was the real shift.

India was not moving from no help to hired help. It was moving from socially arranged help to structurally sourced help. The market was always there. But the modern urban household had become busier, less rooted and more willing to pay to remove friction. The opportunity was no longer just domestic labour. It was what happened when domestic labour met a richer, more mobile and more anonymous India.

10 Minutes to Heaven

While domestic labour itself had not yet been reorganised, the urban Indian consumer had already begun to change.

The trigger came from groceries. Who could’ve thought?

In August 2020, Swiggy launched Instamart. At that point, the promise was still simple: essentials, delivered fast, without the full weekly-stock-up ritual. It was useful, but still felt like a service.

Then the category re-invented itself.

In 2021, Zepto entered with a much sharper proposition: groceries in 10 minutes. It sounded slightly absurd at first. But that was the point. The category stopped asking, “Can online grocery work?” and started asking, “How fast can this become normal?”

A few months later, Grofers became Blinkit. That change was bigger than a rebrand. It was the market announcing that speed was no longer a feature layered on top of commerce. Speed was becoming the product itself. Around that transition, Blinkit said it was already processing over a million orders a week across 12 cities.

By 2022, quick commerce had stopped being a novelty and had become infrastructure for a certain class of urban consumers. As the pandemic hit, delivering essentials fast became essential.

The significance of this was not merely logistical. It was behavioural. Indian consumers have always been willing to wait for many things, especially when the basket size is small and the purchase is habitual. Qcomm altered that trade-off. It showed that convenience could be engineered even for frequent, low-value needs, provided supply density was high enough and fulfilment tight enough.

The market expanded accordingly. Industry estimates place Indian quick commerce GMV at roughly $500 million in FY22 and over $3 billion by FY24. AOVs broadly remained in the ₹400–₹700 range, but frequency did the real work. The same household was no longer placing one large stock-up order and waiting. It was ordered repeatedly throughout the month. That was the real breakthrough. The category proved that low-ticket commerce did not need large margins if it could generate enough habit.

This mattered far beyond groceries.

For the urban household, convenience was no longer an occasional upgrade. It was becoming an expectation. Once milk, vegetables, batteries, cosmetics and medicines could arrive quickly and predictably, the older rhythms of domestic labour started feeling slower by comparison. The watchman, the referral, the number passed around in the building, the follow-up over several days, none of it had disappeared. But it no longer matched the pace of a city that was becoming more responsive.

By 2023, that was the real shift that had taken place.

Qcomm did not solve domestic labour, of course. It made structured, time-bound access feel normal. It had already proved that even low-ticket, high-frequency household needs could be serviced at scale if density, responsiveness and reliability were built into the system.

Snab It

By 2024, the didi economy had begun to look strangely out of sync with the rest of urban India.

The city had changed. The home had not.

Groceries were arriving in minutes. Medicines were arriving in minutes. Small everyday needs that once came with friction had started moving at a very different pace. But the moment a household needed help with sweeping, utensils, laundry or basic cleaning, the city slowed down again. You asked around. You checked with the watchman. You waited for a referral. You called once, then called again.

The labour market was there. What was missing was response time. That is the gap Aayush Agarwal walked into.

In 2024, Aayush was learning the ropes of q-comm inside Zepto, in a business where speed was the whole proposition. Outside work, he was dealing with a much older city. As a working professional in Powai, he was struggling to find reliable home help. He tried the usual routes, online search, agencies, friends, and still found himself stuck in the same manual choreography Indian households had quietly accepted for years.

At one point, the process became difficult enough that his mother flew in from Kolkata to help him find house help. When he started speaking to workers around his own society, the contradiction became obvious. In a complex with hundreds of flats, the supply was there. Access was not.

He wanted to solve this problem, so he called it Snabbit.

It was not built on the idea that India lacked domestic workers. It was built on the idea that Indian cities could no longer coordinate household labour the old way. Snabbit did not begin as a listing product. It began with availability. Workers were organised inside dense residential micro-markets before demand arrived, so chores like sweeping, utensil care, laundry and light cleaning could be dispatched almost immediately.

This is where it breaks from the first wave.

The first wave went after repairs and maintenance, larger-ticket services that showed up occasionally. Snabbit went after recurring household friction. A broken air-conditioner may give you one booking in months. Dirty utensils can give you one tonight.

That makes the model smarter than the first wave. It does not make it easy.

A task worth ₹200 to ₹300 only starts to look meaningful when a worker can do 7 to 8 such tasks a day, pushing daily transaction value towards ₹1,500 to ₹2,000 and monthly worker earnings into the ₹25,000 to ₹30,000 range. The model starts to work only when enough repeat demand is packed tightly within the same geography to keep idle time low.

Snabbit was not digitising the entire didi economy. It is doing something narrower and probably more realistic. It is pulling out one slice of domestic labour that is short enough, standard enough, frequent enough and dense enough, then trying to reorganise just that part.

However, what it has not yet fully shown is whether this speed can be sustained once subsidies fall, competition hardens, and micro-market density must be maintained over time rather than assembled during a land grab.

That is the question a new competitor was trying to solve.

Ready, Set, Pronto

By the time Anjali Sardana started thinking of a return to India, the market had already started whispering something important: this was no longer just a messy labour problem.

It was becoming a real consumer category.

Anjali was a 23-year-old who could easily have pursued a cleaner, more straightforward career in PE, but instead chose one of the most operationally messy categories in urban India - domestic labour.

That choice itself says something.

Pronto was doing something different from Snabbit: it's not building only for urgency. It offered instant, scheduled and recurring bookings, which means it is not just trying to solve the “I need help right now” problem. It was trying to insert itself into the household routine. The problem was being attacked differently.

That distinction matters.

The first wave of home-services startups mostly went after repairs and maintenance - categories that looked large, but behaved poorly because they were infrequent and hard to standardise.

This is a more economical part of the market to build in. The ticket size may be smaller, but the frequency is much higher. In platform businesses, frequency matters more than headline ticket size because it drives habit, repeat usage, and customer recovery over time.

Those numbers suggest this is not just curiosity-led demand. There is clearly real consumer pull in the category.

But the weakness is just as clear.

In this market, booking growth appears earlier than business quality. Convenience gets adoption fast. That does not automatically mean the economics are working. A model like Pronto’s only becomes durable if repeat demand gets concentrated tightly enough within the same micro-markets for worker idle time to fall, utilisation to improve, and margins to tighten without subsidy doing most of the work.

So both readings can be true at once.

The bullish read is that Pronto is building in a meaningfully stronger category than the first wave ever did — one driven by routine, repeat and much deeper household integration.

The sceptical read is that this category still has to prove that fast growth can turn into stable economics once competition intensifies and capital stops absorbing the friction. But a big skeptic had to look at whether this category made sense, because it was existential.

Innovator’s Dilemma

By 2025, instant house-help was no longer something Urban Company could watch from a distance.

Snabbit had already shown that dense availability could quickly create demand. Pronto had shown that this was no longer a one-company experiment. The scale of the two companies was also not trivial.

By February 2026, Snabbit had reached around 8.3 lakh monthly orders, up from roughly 5 lakh in December 2025. In roughly seven months, Pronto from around 1.5 lakh in December 2025 and roughly 3.4–3.5 lakh by February 2026. Neither existed in early 2024.

UC was the innovator, an erstwhile challenger, who was now being challenged. Be the disruptor or be disrupted?

UC’s existing business had been built on a very different kind of category. Beauty, appliance repair, deep cleaning, and grooming were high-ticket, well-structured in execution, and infrequent enough in use to justify training, quality control, and full-stack operations. That model worked. In FY25, Urban Company reported ₹1,144 crore in operating revenue and ₹240 crore in profit.

Instant pulls the company into a very different business.

A beauty customer may book 8 to 10 times a year and spend roughly ₹15,000 to ₹20,000 annually. A domestic-help customer can book 150 to 200 times a year and spend ₹40,000 to ₹60,000. The ticket per task is much smaller. The annual wallet is larger. More importantly, the relationship with the app changes completely. Beauty is a service. Domestic help can become a habit.

The company that owns that habit does not just get more orders. It gets the home.

Urban Company could see that clearly. Its own shareholder updates had already pointed toward cross-sell and newer categories like InstaHelp as the next leg of growth. So it piloted instant help in Mumbai in early 2025 for tasks like cleaning and dishwashing. Within less than a year, the service surpassed 50,000 daily bookings, reaching around 51,520 in a single day.

That proves the need is real, but it also sharpens the problem. The economics still refused to become beautiful. That is the real dilemma.

Urban Company built its moat in categories where standardisation created leverage and margins had room to breathe. Instant help asks for the opposite. Lower ticket. Far higher frequency. Denser labour dependence. Tighter dispatch. Much more pressure on utilisation. Much less room for operational error. Extremely low standardisation or mechanisation.

The scale can look exciting early. The business quality takes longer.

That is why the category’s order numbers need to be read next to its burn. Monthly cash burn across the instant house-help segment reportedly rose from $2 to $3 million in August 2025 to roughly $7 to $8 million by December 2025, with some estimates suggesting it would reach $10 to $11 million per month by February 2026 as competition intensified. Almost 100 Cr a month.

By then, Urban Company’s InstaHelp was at about 8.4 lakh monthly orders, Snabbit at 8.3 lakh, and Pronto at 3.4 lakh.

Demand is real. So is subsidy.

Even frequency, on its own, is not enough. Urban Company has indicated that InstaHelp would need to nearly 2x its average order value to break even. Frequency can drive engagement. It does not automatically solve unit economics if each task remains too small.

So why enter at all? Because the real threat is not that Snabbit or Pronto replace beauty or repairs overnight. They are going after the home. That is why instant help is not just expansion. It is a defence.

Urban Company may not be entering this category because it is the cleanest business on offer. It may be entering because it is too strategically important to leave to someone else.

That is what makes this moment uncomfortable. The category with the messiest economics may also become the one with the strongest hold on the home.

It’s the Economics, Stupid

The deep question is - can any platform build a version of domestic labour that is better than the old system after the discounts fade, the burn slows, and the density has to sustain itself?

Formalising an informal economy also adds costs, like GST and digitisation. Sometimes the informality of the system is what makes the economics work.

The old system, for all its messiness, already does something very hard. It clears labour with almost no visible coordination costs, and it does so in a way deeply adapted to how Indian homes actually function.

The startups have already proved one thing. Domestic labour can be made faster. They have not yet proved the thing that matters more, that it can be made structurally better at scale. They also have to deal with safety issues arising from the platforms' absolute anonymity.

That is what will decide whether this becomes the operating system of the Indian home, or just another venture-funded layer manufactured to sit on top of a market that was already working.

It is clear that India’s domestic labour market may be informal, but it is not empty or stupid.

It already gives households something platforms still struggle to fully reproduce: continuity, flexibility, memory, and a long-term working relationship, with very little visible overhead. A regular worker may not arrive in ten minutes, but she knows the house, the family, the routine, the adjustments. The system is messy, but it is deeply adapted to how Indian homes actually function.

This market will not be decided by whether consumers like apps. They clearly do. It will not be decided by the existence of demand. That part is now beyond doubt. It will be decided by whether platform-mediated domestic labour can consistently produce a better economic outcome than the old system, not once during a funding cycle, but repeatedly, durably, and after the subsidy starts disappearing.

That means better for both sides.

Better for the worker in the form of higher take-home earnings, more reliable utilisation, shorter travel, and less dependence on informal volatility. Better for the household in the form of predictable access, lower search friction, and enough trust to make repeat usage natural rather than forced. If platforms can do that while still carrying the weight of commissions, support, and operations, then the didi economy may not remain just another labour category. It could become the organising layer through which India’s entire home-services market is accessed.

But if they cannot, the old network will continue to win for the same reason it has always won.

It already clears labour with almost no visible coordination cost. It does not need CAC. It does not need discounting. It does not need a city launch strategy. It runs on proximity, reputation, repetition and adjustment. In startup language, it still looks unorganised.

In economic language, it remains one of the most efficient labour-matching systems in the country. Whether this layer adds more efficiency, or distorts the market momentarily, is what the next few years will reveal in the three horse race.