Is India's $100B Solar Market a Giant Hiding in Plain Sight?

B2C

B2B

Series A

Last fortnight, Delhi hit 47 °C and India broke peak power demand records across five states, while a country that ran on diesel generators and 16-hour power cuts not 20 years ago has crossed 100 gigawatts of solar

A Country Full of Sunlight, Running on Diesel

In the early 2000s, India’s electricity problem had become so normal that people had stopped treating it like a crisis.

Power cuts had a timetable. Families planned meals around them. Shopkeepers knew when to switch on the inverter. Factory owners knew how much diesel had to be stocked before the machines stopped.

Across the country, peak demand was running 12 to 15 per cent ahead of supply. In Bihar and Uttar Pradesh, the lights could be out for 14 hours a day. In Gujarat and Maharashtra, some of India’s largest industrial belts were no longer running solely on grid power. They were running on a second electricity system built from diesel generators, fuel bills, and backup planning.

That was the strange starting point of India’s solar story.

A country with more than 300 sunny days across much of the map was still burning diesel to survive its power shortages.

Nowhere was this contradiction sharper than in Rajasthan (ironic, as it gets buried in most solar origin stories) - the state that would eventually become the world's largest solar park hub was, in the early 2000s, among India's most power-deprived. The sun fell on Rajasthan for 325 days a year. Temperatures in Jodhpur crossed 50 degrees in summer. The electricity infrastructure was too broken to capture any of it.

The sun was abundant, but reliable electricity was not.

But even if someone wanted to convert that sunlight into power, the economics did not yet work. Solar power costs ₹12 to ₹18 per unit. Coal power was available at ₹2-₹3. For a country already short of electricity, solar looked less like a solution and more like an expensive experiment.

The price was only the first problem; the deeper problem was the grid itself.

State distribution companies were drowning in political tariffs, incomplete collections and chronic losses. Across most state utilities, aggregate technical and commercial losses were above 30 per cent. In some states, they crossed 40 per cent. In simple terms, a large part of the electricity generated in India was either lost, stolen, under-billed or never paid for.

Even if a private company built a solar plant, the harder question remained. Who would buy the power, at what price? And would they pay on time?

That one question would haunt India’s solar market for the next two decades. Every developer who entered the sector eventually met the same wall: weak DISCOMs. Some survived it. Many did not.

A few companies began testing the edges. Orb Energy started in Bangalore in 2006, selling solar to rural households through microfinance partnerships. Azure Power made the early case for utility-scale solar in 2008, before any government auction had confirmed its commercial viability. Neither company was building a market. They were proving something was possible. It would take years for anyone to fully act on that proof

India was already the fifth-largest energy consumer in the world. It had rising demand, chronic power shortages, factories running on diesel and some of the best solar conditions on the planet.

On paper, it looked like the perfect market for solar power, but in reality, it was one of the hardest places in the world to build it. Because before India could scale solar, it first had to solve a more basic problem: how to make electricity itself a functioning business.

The Bid Awakening

In January 2010, Prime Minister Manmohan Singh announced the Jawaharlal Nehru National Solar Mission. Target: 20 gigawatts of solar by 2022. At the time, India had less than 20 megawatts of installed capacity. The ambition was not incremental. It was a signal that the rules had changed.

The Solar Energy Corporation of India started running competitive auctions. Developers bid on the tariff they would accept per unit. Lowest bid wins. First rounds came in at Rs. 10-12 per unit. Then they started falling.

Rajasthan and Gujarat became the proving grounds. Flat land, high irradiation, and available government parcels. Bhadla, a patch of desert in Jodhpur district where summer temperatures crossed 50 degrees Celsius, was identified early as a flagship site. It looked inhospitable. It would eventually become the world's largest solar park, with over 2.7 gigawatts of installed capacity across four phases.

The conglomerates came. Adani entered early and built aggressively. Tata Power Solar, which has been manufacturing panels since the 1980s, moved into project development. NTPC took solar on as a mandate, not a side project. Azure Power grew with every auction round. CleanMax Solar, founded in Mumbai in 2011, began signing long-term PPAs with factories and corporate campuses, demonstrating that the appetite for solar extended well beyond government contracts.

By 2014, average winning tariffs had fallen to roughly Rs. 5 per unit. Less than half of four years ago.

Two cracks were visible in 2015 to anyone paying attention. India was buying almost all its panels from China. No domestic manufacturing capability worth mentioning existed. The entire mission was being built on imported hardware. And the DISCOMs signing those offtake agreements were already defaulting on payments. Projects commissioned in 2013 and 2014 were waiting months to get paid. The market was growing on the surface. The structural problem was compounding underneath.

Yuan for the Money

Between 2010 and 2015, China was doing something that would reshape every solar market on Earth. Not just building factories. Wiring an entire industrial policy around making solar panels the cheapest manufactured product in history.

The China Development Bank extended $20 billion in financing to domestic solar manufacturers in 2010 alone. Provincial governments competed to attract solar production, backing credit lines, offering land, and guaranteeing loans. Local officials were measured on growth numbers. Solar factories delivered growth numbers. The result was a capacity that grew far faster than demand, and a mandate to export the excess. Global panel prices fell from $4 per watt to under $0.40. A Chinese module ended up 50 per cent cheaper than a European one and 65 per cent cheaper than one made in America.

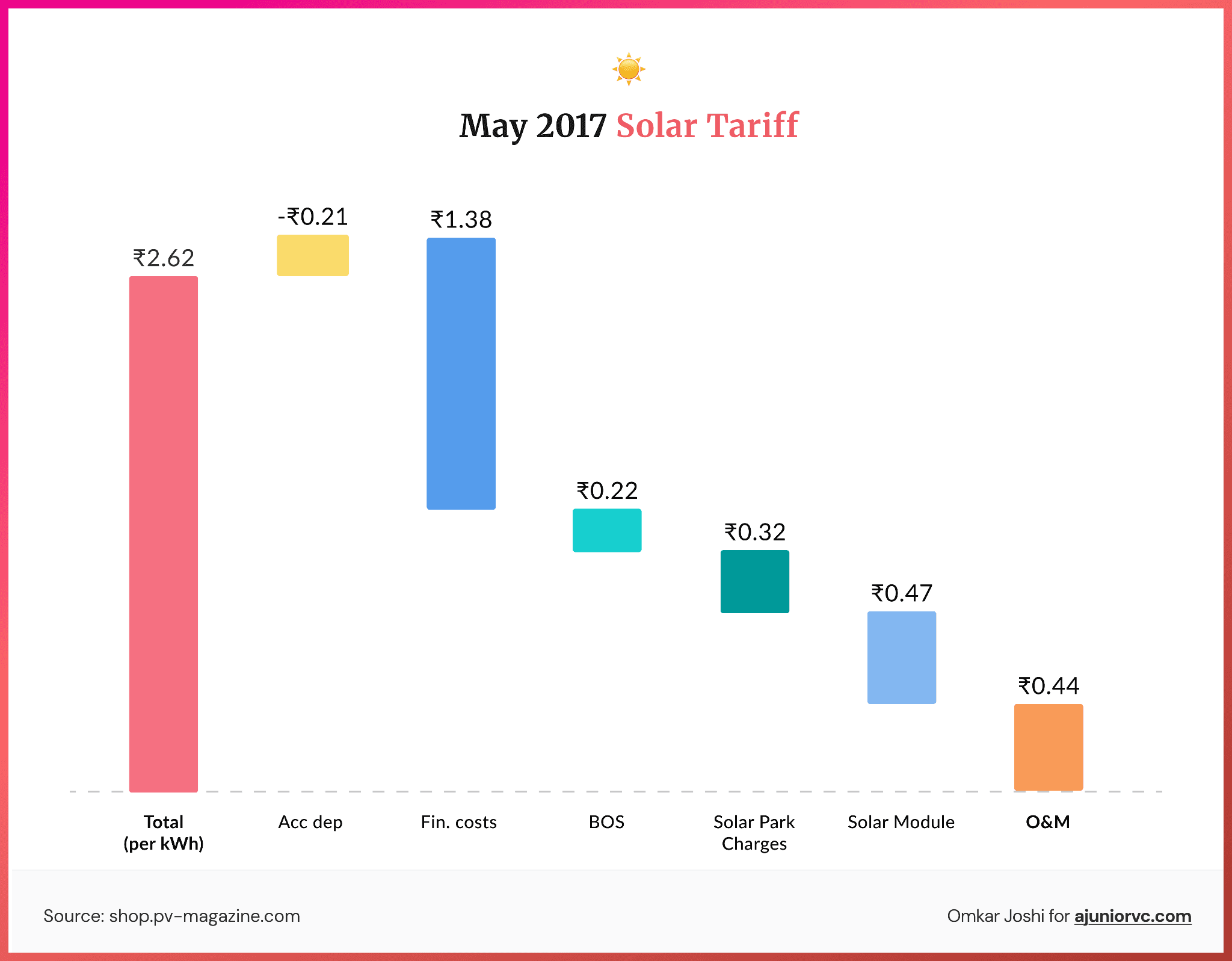

India benefited more than almost anyone. At a SECI auction in May 2017, ACME Solar bid Rs. 2.44 per unit for Phase III of the Bhadla Solar Park. Hero Future Energies came in at Rs. 2.45. The world's lowest recorded solar tariff. The headline went global within hours.

The problem did not travel with it.

At Rs. 2.44, every cost overrun, every delayed shipment, every shift in the rupee-dollar rate could entirely break the project's economics. Within weeks of winning at Bhadla, Chinese module prices reversed and began rising. ACME had to file for an IPO to raise the capital needed just to execute the project. A separate 600 MW project in Rajasthan, won at similarly aggressive rates, was eventually cancelled outright. Average tariffs had dropped 73 per cent between 2010 and 2017. What that number did not show was how many developers were quietly renegotiating construction timelines with lenders.

The race to the bottom on tariffs had made India's solar growth look spectacular while weakening the financial health of the companies building it.

Indian manufacturers had no shelter from the storm. Waaree in Gujarat and Vikram Solar in Kolkata were producing panels, but at prices that couldn't touch Chinese imports. India's import dependence climbed to 80-90 per cent. The government could see the problem. Acting on it would push tariffs higher, and higher tariffs made bad headlines. Cheap Chinese panels were what was making the mission's numbers look good.

The side effect nobody had planned for: rooftop solar had just become economically viable for the first time. A handful of entrepreneurs started doing the math.

Permission Impossible

Net metering arrived on paper in 2013.

By 2018, most states had some version of the policy in place. What followed was not a market opening. It was a bureaucratic obstacle course, state by state, DISCOM by DISCOM.

Rules were different everywhere, caps set so low that they limited the size of systems anyone could install. Approvals that dragged on for months and policies revised multiple times over three years. An installer operating across Maharashtra and Rajasthan faced two completely different regulatory realities. The National Solar Mission had a target. The states had their own agendas.

The deeper resistance came from the DISCOMs themselves.

For a state electricity board already running a deficit, every rooftop system installed was a unit less sold. Their revenue model depended on consumption. Rooftop solar attacked that model directly. So DISCOMs did what institutions do when their revenue is threatened. They slowed things down. Added technical requirements. Made the approval process so exhausting that households gave up before making a purchase decision.

Commercial and industrial rooftop found a way through. CleanMax and Amplus Solar built serious businesses, signing long-term PPAs with factories and office complexes. The economics were strong enough, and the customers experienced enough, to push through the friction.

Residential was a completely different problem.

A household wanting to go solar needed to find a trustworthy installer in a market full of untrustworthy ones. Unqualified operators had entered solar because panels were cheap and margins looked easy. They sourced second-hand stock. Installed systems that degraded within two years. Collected advance payments. Went unreachable. The fraud alerts were being published openly: contractors collecting "subsidy fees" and vanishing, customers left with neither panels nor refunds.

Then there was the awareness problem that nobody talks about. A significant share of urban households confused solar panels with solar water heaters. Two different products. Two different functions. Entirely different outcomes. Residential solar companies spent the first half of a sales conversation explaining what they were actually selling.

The opportunity was real, but the market was, well, horrible!

The Roof Breaks Even

Nobody planned for COVID to become a trigger for solar sales. It did.

The lockdown moved electricity consumption from offices and factories into homes. Bills arrived in April 2020 in numbers those households had never seen. Enquiries to solar installers started spiking in the same weeks. The demand was always latent. It took sitting at home, watching the meter run, to make it visible.

The structural barrier was never awareness. It was financing.

NBFCs and a few private banks began developing solar-specific loan products through 2020 and 2021. The math, once someone worked it out, was simple. A rooftop system financed over five years produced an EMI lower than the household's existing monthly electricity bill. From day one, consumers spent less than they were spending before. They didn't need Rs. 4 lakh idle. They needed to decide whether paying less every month from now on made sense.

The buyer profile changed almost immediately.

The people adopting residential solar in 2021 were not wealthy households deploying idle capital. They were salaried and urban, running a monthly savings calculation. Companies that understood this rebuilt their sales process around the EMI narrative. The conversation shifted from kilowatt hours and panel specs to payback periods and monthly savings. VC money followed the demand signal.

India was simultaneously becoming the second-largest market globally for corporate renewable PPAs. Microsoft purchased 437 MW of solar and wind capacity from ReNew in India. Amazon signed wind PPAs. Large Indian corporations made long-term green energy commitments for the first time at scale. The institutional credibility the sector had lacked was starting to arrive.

Tata Power Solar entering the residential market in this period carried its own meaning. When a company with that balance sheet and that brand takes a consumer segment seriously, the segment has arrived.

All That Glitters

India added roughly 14 gigawatts of solar capacity in 2022, and for the first time in years, the sector did not appear to be surviving solely on policy ambition.

Capital was moving in, residential rooftop was seeing real transaction volumes, developers were bidding aggressively, and manufacturers who had spent years fighting cheap imports were suddenly being viewed as strategic assets.

The sector finally looked like it had found its footing. Then came the Approved List of Models and Manufacturers, or ALMM.

The logic was hard to ignore. India was still 80 to 90 per cent dependent on Chinese solar panels. One supply shock, one policy change in Beijing, one geopolitical escalation, and a large part of India’s solar mission could slow down for reasons completely outside India’s control.

ALMM was meant to reduce that risk by ensuring that solar projects linked to government schemes used only panels from approved domestic manufacturers. The direction made sense. India could not build one of the world’s largest solar markets while depending on imported hardware for its most critical component.

The problem was that policy moved faster than domestic capacity.

Indian manufacturers could not immediately absorb the volume redirected to them. Approved panels became scarce. Mono-PERC module prices moved from around $0.18 per watt toward $0.28 per watt, and over 18 months, module costs rose by more than 40 per cent.

For developers, this was not a normal cost increase.

Solar projects are bid, financed and contracted on narrow assumptions around module prices, tariffs, debt costs and timelines. Once panel prices move sharply after a bid has already been won, the whole return profile changes. Timelines slip. Contracts need renegotiation. Projects that looked viable at the bidding stage begin to carry execution risk.

Nearly 4.4 gigawatts of already-auctioned capacity faced return pressure because module prices had moved beyond what those bids could absorb.

That was the trade-off India had walked into.

The country needed domestic manufacturing to reduce its dependence. But the market still needed affordable panels to keep projects moving. For a while, both priorities were pulling in different directions.

The pressure, however, also created a second-order opportunity.

Waaree, which had spent years competing with Chinese imports inside India, began finding buyers in Europe and early traction in the United States. The same global anxiety about China that pushed India to rethink its supply chain was also prompting other markets to seek non-Chinese suppliers.

That changed how the manufacturing story was being read.

Orb Energy raised a Series D targeting $48 million. Waaree filed for its IPO. Rooftop solar was moving beyond early-adopter homes in large metros into Jaipur, Surat, Coimbatore, Nagpur and other Tier 2 cities where electricity bills were high enough, roof ownership was common enough, and the payback period was easier to justify.

But expansion made the business more local, not cleaner.

Every new city brought a different DISCOM, the local electricity distribution company that controlled approvals, billing and net metering. Every DISCOM had its own process, and every process added a different kind of delay.

So the category was expanding, but the friction was expanding with it.

Solar had started looking inevitable but was far from easy.

Sunburn

By FY23, India’s solar boom had reached the point where demand wasn’t enough.

The sector still had capital, policy ambition and long-term demand, but it was now facing a rare three-way squeeze: higher module costs, delayed DISCOM payments and weaker rooftop returns. The stress was not just visible inside the sector. It showed up in capacity additions. Solar installations fell 44 per cent in 2023, from 13.4 GW in 2022 to 7.5 GW. Utility-scale solar was hit even harder, falling nearly 51 per cent in the same period.

Everything that had looked manageable during the boom became harder once the market started scaling.

The first place the squeeze showed up was in panel costs. Import duties on Chinese panels remained at 40 per cent, while ALMM-compliant domestic supply still could not meet total market demand. Projects that had been underwritten at one module price were suddenly being built at another. Timelines stretched, contracts reopened, and returns that looked reasonable at the bidding stage started getting squeezed during execution.

This was not a normal input-cost increase because solar projects are built on narrow assumptions: module price, tariff, debt cost, commissioning timeline and expected return. Once panel prices move after a bid has already been won, the project does not just become less profitable. The entire return profile changes.

Then the old DISCOM problem returned at a scale that could not be managed quietly. By June 2022, state electricity boards owed power generators nearly ₹1.39 lakh crore in legacy dues. For developers, this was not an abstract government balance-sheet problem. These were payments they had already built into their working capital assumptions. Projects had been commissioned assuming a certain payment cycle, and that cycle never fully arrived.

The stress shifted from policy to cash flow, just as rooftop solar was facing a quieter but equally damaging problem. In simple terms, net metering decides how much credit a rooftop owner gets for the excess electricity sent back to the grid. Once those credits, caps or approval terms change, the customer’s payback period changes too.

That mattered because rooftop solar was being sold on a simple calculation: install today, save on bills, and recover the cost over a predictable number of years. Once that payback calculation became uncertain, the entire sales pitch weakened.

For residential solar companies, this came at the worst possible time. The financing wave of 2021 and 2022 had helped many rooftop companies scale quickly, but scale alone had not fixed the business. A rooftop sale was not just a digital lead. It needed site visits, structural checks, financing follow-ups, DISCOM paperwork, installation teams, post-installation servicing and years of warranty support.

Many companies had closed transactions at volume without fully pricing in the cost of serving those customers over the life of the system. Growth did not hide the unit economics anymore. It exposed them.

Then consolidation began. The weaker players ran out of runway. Some shut down, some got absorbed, some simply became unavailable to customers who still had 20-year systems sitting on their roofs.

That was the painful irony. The trust problem in rooftop solar did not return through the old fly-by-night installer of 2018. It came back through a newer version of the same problem: the venture-backed rooftop company that raised in 2021, scaled in 2022, and was no longer around when the customer needed support in 2024.

The Century

India’s solar capacity scaled from roughly 20 MW to more than 100 GW in just 14 years, a 5,000x expansion that few energy markets worldwide have matched.

The original Jawaharlal Nehru National Solar Mission target was 20 GW by 2022, a number that had drawn polite scepticism when it was announced in January 2010. India did not just meet that target. It built five times that capacity two years later and became the world's third-largest solar market, behind only China and the United States.

But the 100 GW milestone also created a new question.

After utility-scale parks had carried the first phase of India’s solar buildout, where would the next layer of growth come from?

For most of its life, Indian solar had been a large-project story: solar parks, auctions, developers, power purchase agreements and state utilities. The consumer was present in the story only indirectly, as the person receiving electricity through the grid.

By 2024, that started changing. The next layer was coming from rooftops.

India installed 3.2 GW of rooftop solar in 2024, an 88 per cent jump from the previous year. Residential consumers drove 74 per cent of that capacity. To put that in perspective, rooftop solar added in one year was 160 times larger than India’s entire solar capacity in 2010.

In the first six months of 2025, another 4.9 GW came online. Half a year of rooftop additions was more than 245 times the solar capacity India had when the national mission began.

This was no longer only a capacity story. It was becoming a household adoption story.

For years, rooftop solar had been stuck between interest and action. People liked the idea, but the process felt heavy. Subsidies were confusing. Financing was limited. Installers were uneven. DISCOM approvals were slow. The savings made sense, but the effort did not always feel worth it.

PM Surya Ghar changed the shape of that funnel.

Launched in February 2024, the scheme received 47 lakh applications in its first year. By March 2025, 10 lakh homes had been solarised under it. By December 2025, that number had crossed 19 lakh.

For context, Germany, Europe’s solar leader, took nearly two decades of aggressive green energy policy to reach 5 million residential solar installations. India was still behind in absolute penetration, but the speed had changed completely. It was no longer building rooftop solar on a European timeline.

It was trying to compress household adoption into a very Indian one. The supply side was also catching up.

The manufacturing gap that had hurt the sector through 2022 and 2023 was finally being attacked with real capacity, not just policy intent. Waaree commissioned a 5.4 GW solar cell facility in Chikhli, Gujarat. Tata Power Solar commissioned a 4.3 GW integrated cell-to-module facility in Tamil Nadu. The import dependency that had made the sector vulnerable was still not fully gone, but it was no longer being accepted as a permanent condition.

Waaree’s IPO captured that shift better than any policy document could.

The issue was priced at ₹1,503 per share and listed on the BSE at ₹2,550 on October 28, 2024, a 70 per cent premium on day one. It was subscribed to 76 times. For years, solar manufacturing had been treated like a fragile, policy-dependent business that struggled against Chinese imports. That listing showed a different mood: investors were beginning to treat solar manufacturing as a capacity story India could finally own.

The utility-scale side had matured, too. Adani Green crossed 12 GW of operational capacity. Azure Power continued to hold a portfolio above 4 GW. The large-project architecture that India had spent more than a decade building was now in place.

But this chapter was different because the missing consumer layer had finally begun to assemble.

For the first time, a homeowner was not being asked to carry the entire solar decision alone. Banks had loan products. NBFCs had financing options. Government subsidies reduced the upfront hit. Zero-cost EMI made the decision easier to digest. Installers had become more organised. A household in Pune or Chennai could compare providers, check financing, claim subsidy and get a system installed in a way that would have felt almost impossible a decade earlier.

This is where SolarSquare entered.

The company started as a small B2B installer in 2015, pivoted to residential, and survived the phase when rooftop solar looked attractive on paper but proved brutal in execution. In FY24, it was still spending ₹1.31 for every rupee of revenue, a reminder that the category had not magically become easy.

Yet the company was about to raise at a valuation of $450 million to $500 million, with B Capital and Lightspeed Venture Partners in discussions to lead the round. That valuation did not appear because rooftop solar suddenly became fashionable. It appeared because the surrounding market had finally started to look complete.

JNNSM built the policy foundation. China, ironically, helped bring down global panel prices. Indian manufacturers began adding serious domestic capacity. Lenders built consumer financing. PM Surya Ghar created a national demand funnel. Rising electricity bills made the household calculation sharper.

SolarSquare was not rising into the same market that existed in 2015. It was entering a market that had survived trust issues, supply shocks, margin compression, DISCOM delays, and policy confusion, and was still moving.

That is what changed between 2010 and 2026. The transformation was never just about adding gigawatts.

India did not simply build more than 100 GW of solar capacity. It assembled the ecosystem required to sustain it: policy that created direction, manufacturers that added domestic capacity, financiers that reduced friction, and consumer programmes that turned interest into adoption.

The achievement was not the panels alone. It was the creation of an infrastructure, industrial, financial and behavioural, that made solar feel less like an ambitious transition and more like an inevitable part of India’s future.

Second Sun

India crossing 100 GW makes the story look mature.

The strange part is that the largest solar market inside India is still barely built. CEEW estimates India has 637 GW of residential rooftop solar potential, enough to cover more than 25 crore households. Tapping even one-third of that potential could support the entire electricity demand of India’s residential sector. Against that, what India has installed so far is still a fraction.

The utility-scale story has matured. The harder chapter now sits on rooftops, where every sale is smaller, more local, more operationally messy, but also much closer to the consumer.

Storage is what can change the shape of that market.

Without storage, rooftop solar is mostly a bill-saving product. It generates during the day, reduces grid consumption, and sends excess power back through net metering. Useful, but still limited by when the sun is producing and how the grid credits that power.

With storage, the product becomes much harder to ignore.

Battery storage costs fell 40 per cent in 2024 and another 31 per cent in 2025. Solar-plus-storage bids in India are already landing at ₹3.1-₹3.5 per unit in some tenders, and the curve is still falling. Once storage becomes affordable for residential users, a rooftop system is no longer just about lowering the electricity bill. It starts to become backup, reliability, and control.

That matters because Indian households are about to consume more electricity, not less.

EV charging changes the calculation further. A household that charges a two-wheeler or four-wheeler every day no longer views electricity the same way. The home becomes a small energy system: appliances, cooling, backup, mobility. A rooftop system sized for both home power and vehicle charging gives the consumer a stronger reason to install and the installer a larger product to sell.

This is where the market moves beyond the obvious homes in Bengaluru, Mumbai, Pune and Chennai.

In high-tariff urban markets, rooftop solar is sold on savings. In Tier 2 cities, it will depend on financing, installer trust and smoother approvals. In semi-urban and rural markets, the pitch may shift from the monthly bill to reliability: fewer outages, less dependence on voltage swings, and, eventually, the ability to store power when the grid fails.

That is why India’s remaining rooftop opportunity will not be unlocked by cheaper panels alone.It will need storage, financing, local installers and DISCOM cooperation to move together.

The DISCOM problem has not disappeared. Legacy dues have come down from the ₹1.39 lakh crore peak in June 2022, but the incentive conflict remains. A utility whose revenue model depends on selling centralised power will always have a complicated relationship with households that want to generate their own.

That is the real bottleneck now.

India has already proved that it can build solar capacity at scale. The next question is whether it can build a distributed solar market without making the local utility feel like the loser in the transaction.

More than 600 GW of residential rooftop potential is still sitting on Indian homes.

Whether India unlocks it in 10 years or 30 will depend on the same problem that has been hiding inside this story from the first paragrap - the grid