Can ₹6,000 Cr Shadowfax Solve a Problem Amazon, Swiggy and Blinkit Still Can’t Crack?

Logistics

Last month, Shadowfax filed for a ₹2,000 crore IPO, in line with many companies from its vintage going public.

Blind Spots

In 2015, India’s logistics system was optimised for long-distance movement, not last-mile variability.

Large courier networks handled intercity transport efficiently, but intra-city delivery performance diverged sharply. The problem was structural. Fixed-route, fixed-shift operations could not respond to India’s hyperlocal complexity.

Address density, informal landmarks, unplanned layouts and inconsistent customer availability created high friction in the final 500 metres. A non-local delivery agent spent disproportionate time on navigation, reducing utilisation and increasing cost. This inefficiency was visible across hostels, PGs, apartments and urban colonies.

At IIT Delhi, this showed up daily for restaurant orders.

Agents queued at the hostel gate, made multiple calls and completed fewer deliveries per hour than operationally viable. For two IIT Delhi grads, Abhishek Bansal and Vaibhav Khandelwal, the pattern pointed to a simple conclusion. The bottleneck was not logistics capacity but local knowledge.

Informal gig workers - students, migrants, part-time earners - had higher familiarity with neighbourhood layouts. They made faster decisions and required less navigational assistance.

The founders tested this hypothesis by activating a small supply pool inside the campus. The performance difference was clear: lower delivery time, fewer failures and higher customer satisfaction.

The insight was straightforward.

India’s last mile operates more like a local information market than a standardised logistics market. Efficiency depends on the agent’s familiarity with micro-geography, not just routing tools.

India’s logistics network was built to move parcels across states, not across neighbourhoods.

A package could travel reliably from Delhi to Bangalore. The final three kilometres were unpredictable. Vague addresses, locked gates, COD behaviour, and return rates that were structurally higher than global benchmarks.

For years, this friction sat in plain sight. But when India’s commerce shifted online, the mismatch became impossible to ignore. Abhishek and Vaibhav were onto something.

Last-Mile Hole

The last mile didn’t fail due to poor technology or weak operations.

It failed because it wasn’t designed for how Indian cities actually function. The duo began Shadowfax as an attempt to turn everyday familiarity, the knowledge riders already carried, into a scalable operating model. Named after Gandalf’s horse in Lord of the Rings, it was known for being speedier than the wind.

At the same time, the country already had a latent supply of flexible labour. Students, shift workers, and under-employed two-wheeler owners were willing to take short-duration gigs with predictable payouts.

This was a natural fit for a variable-demand environment.

Shadowfax organised this supply into a lightweight fulfilment layer. The model shifted the cost structure away from fixed labour to variable utilisation. If demand spiked, more riders could activate. If demand dropped, the system contracted automatically.

This flexibility matched India’s volatile consumption cycles. Higher on weekends, festivals and sales, lower on other days.

By mid-2015, early operations showed that pooled hyperlocal delivery was feasible. Riders completed more tasks per hour because they were already familiar with the area. Merchants received predictable SLAs, improving repeat usage. The company avoided heavy asset investment, reducing breakeven thresholds.

The early learning was that unit economics in the last mile were driven by density, familiarity and utilisation. Traditional courier networks were strong on density but weak on familiarity and utilisation. Shadowfax’s model improved the latter two without compromising the first.

Another observation emerged: multi-category routing further increased utilisation. A rider who completed a food order could immediately take a parcel pickup or pharmacy run. While not yet engineered as a complete pooling engine, the pattern suggests that hyperlocal supply could be shared across verticals to achieve better cost curves.

By the end of 2015, the company was still small but had validated three principles. The last mile is a variable-workforce problem, not a fixed-route problem. Local familiarity reduces delivery time more than pure navigation technology, and multi-category work increases asset productivity at low marginal cost.

These principles became the foundation for the next phase of scaling.

Shadowfax had not yet integrated with large platforms, but the operational blueprint was visible. A flexible, hyperlocal, tech-coordinated network that could deliver significant cost advantages over legacy models.

The company had also identified which parts of logistics incumbents could not adapt to quickly. They struggled with unpredictable demand, high-scatter delivery zones, and low-density return pickups. This gap, structural rather than temporary, became the company’s long-term wedge.

By the end of the year, Shadowfax had demonstrated that India’s last mile required a human-capital-first, tech-orchestrated approach.

Delivery Market Fit

By 2016, food delivery platforms were expanding rapidly.

Their operational constraints mirrored those visible in campus deliveries: high frequency, short distance and tight time windows. Legacy courier networks were not designed for these characteristics. Their cost models depended on batch consolidation and scheduled routes.

Shadowfax’s flexible pool aligned more naturally with Swiggy’s early requirements. Given its restaurant focus, they also had the right understanding of the space.

Local familiarity reduced per-order navigation time, increasing rider utilisation. In dense micro-zones, riders achieved 2.0–2.4 orders/hour compared to the 1.2–1.5 orders/hour typical of non-local or fixed-shift networks. The improvement came primarily from reduced lookup time and route switching.

This period established early product-market fit.

The same supply base could also handle pharmacy and grocery deliveries with minimal additional training. Hyperlocal categories shared similar distance bands and service expectations.

Flipkart began exploring enhancements in its last-mile and reverse logistics operations at the same time. Returns posed a structural challenge. They were scattered, time-uncertain and expensive under fixed-route networks. Traditional couriers treated returns as low-priority loads. SLA variability was high.

Shadowfax’s variable-cost model provided a better match.

Riders could perform reverse pickups opportunistically along micro-routes. A return pickup that cost ₹75–₹90 on rigid networks often fell to ₹50–₹65 under Shadowfax due to pooled routing and higher labour elasticity.

Two themes emerged during late 2016 and early 2017. Food delivery created predictable density, and returns created utilisation during low-demand hours. The combination stabilised riders' earnings and improved network throughput. Multi-category utilisation became a structural advantage.

The tech stack matured in this period. Allocation moved from manual dispatching to automated matching driven by proximity and workload. Routing began incorporating early batching logic. These upgrades were incremental but meaningful. They aligned the system with actual demand patterns rather than theoretical optimisation.

The company expanded beyond Delhi NCR into Bangalore. The operating structure translated cleanly. Food for density, returns for utilisation, e-commerce forward for scheduled evening flows. The interplay of these segments generated a stable throughput profile.

Comparisons with other hyperlocal startups were instructive.

Roadrunnr, Opinio and others attempted category-specific models. Their utilisation curves were volatile. Idle time increased the cost per order. Shadowfax’s multi-category design smoothed demand variability. It became clear that single-category hyperlocal models were structurally fragile in India.

Rider payout design also evolved. Predictable earnings attracted more reliable suppliers. Reliability improved SLA performance. Stronger SLAs unlocked more enterprise integrations. This created a reinforcing cycle that incumbents found difficult to match.

By late 2017, Shadowfax was handling food, e-commerce returns, pharmacy and grocery deliveries across multiple cities. The company remained largely invisible to end consumers, but enterprise operators increasingly recognised the efficiency gap.

The lesson from this era was that India’s last mile is a multi-category utilisation challenge, not a fleet-expansion challenge. Legacy networks could not adapt because their cost structures and operational incentives were built for scheduled loads, not elastic multi-category fulfilment.

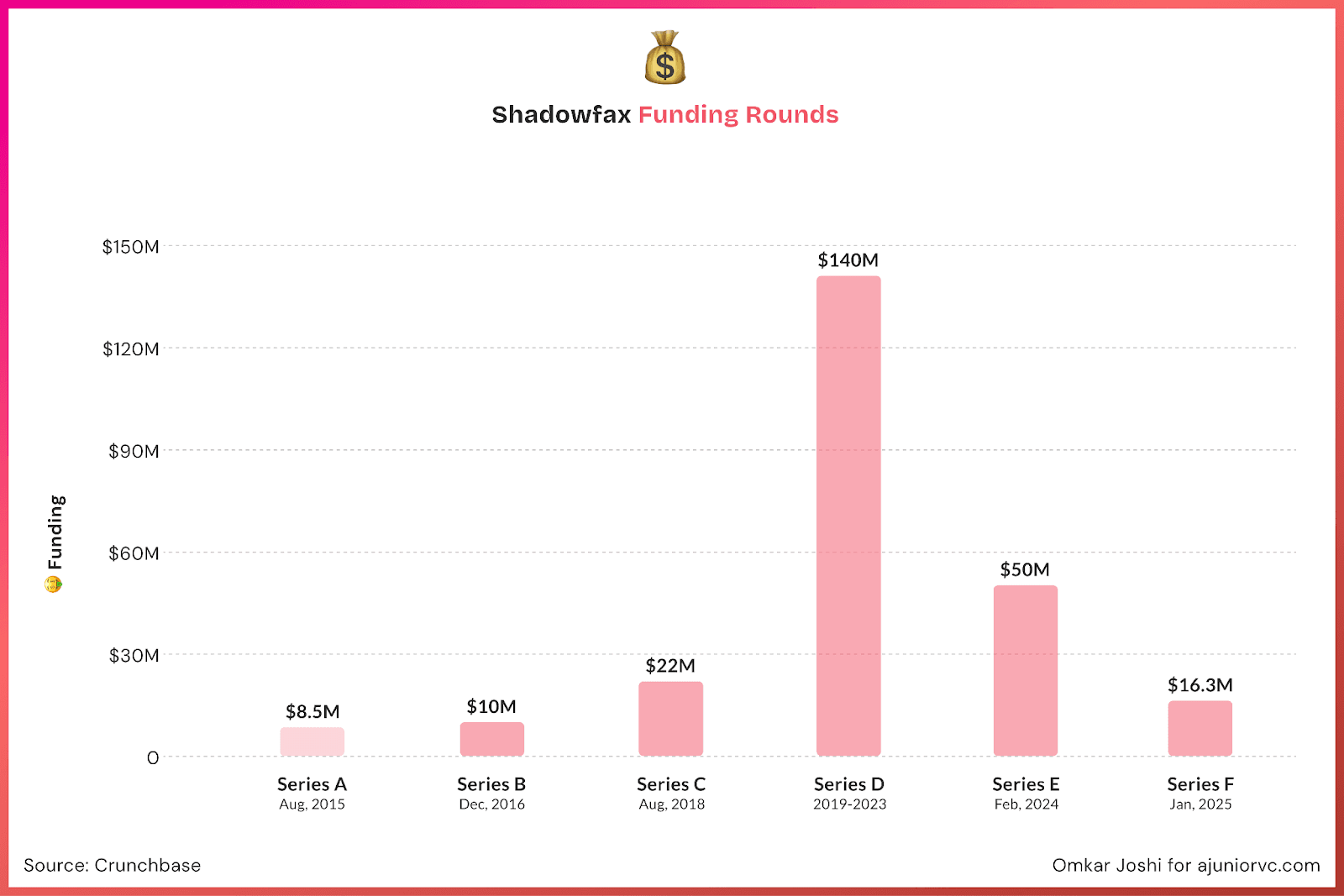

This period locked in the company’s differentiation. It proved that a non-asset, variable-cost labour network could outperform incumbents across speed, reliability and cost in the last mile. It ended up raising a $10M Series B round, in quick succession from its Seed and Series A.

Elastic Supply Infrastructure

Between 2017 and 2019, India’s shift toward hyperlocal consumption became more visible.

Consumers began ordering groceries, medicines and low-ticket essentials online, not out of habit but out of convenience that felt increasingly normal. This pattern changed the expectations placed on logistics networks. Fulfilment had to be fast, predictable, and flexible, and most existing courier structures were not built for this level of variability.

Shadowfax’s network adapted more naturally because it was designed around flexible labour and local familiarity. When the company expanded into grocery and pharmacy deliveries, riders already understood the neighbourhoods they served.

They knew which shops opened late, which societies had strict entry rules and which lanes cut travel time. These small human advantages translated into more predictable delivery times.

Category expansion also stabilised utilisation. Grocery brought planned demand, especially during mornings and early evenings. The pharmacy added a steady stream of mid-day orders that riders could complete quickly. E-commerce forward shipments created concentrated evening peaks. None of these categories individually could support an efficient labour pool, but together they formed a day-long rhythm that reduced idle time.

BigBasket and 1mg were pivotal in shaping this.

Riders became used to switching between categories, and the system learned to allocate orders based on familiarity and distance rather than rigid routing rules. Meesho added another layer altogether: high-volume, low-ticket goods from tier-2 and tier-3 sellers, which blended into the existing network with minimal friction.

Riders treated these orders the same way they treated local pickups; they simply extended their routes into new pin codes.

As volumes increased, Shadowfax invested in creating a more dependable supply engine. Onboarding became smoother. Payout cycles became more predictable. The company learned that riders valued stability as much as earnings, and that small changes, such as faster dispute resolution or transparent earnings panels, improved retention. Better retention improved SLAs, which made enterprise partners more willing to scale with the company.

The routing layer matured in parallel.

Early systems were basic, focusing on proximity. Over time, dispatch decisions incorporated micro-batching and clustering logic. Riders were assigned multiple orders in tight radii, cutting down travel distance. The improvements were subtle but material; each saved minute compounded across tens of thousands of daily orders.

Expansion beyond Delhi NCR and Bangalore followed a disciplined pattern.

The company entered new cities by focusing on a few high-density pockets, proving utilisation, and only then widening coverage. This approach prevented margin dilution in early months, a problem that had affected several hyperlocal startups that expanded too quickly without density logic.

Semi-urban and rural expansion brought new operational behaviour. In many of these regions, local riders already acted as informal couriers for kirana shops or medical stores. Shadowfax simply formalised this behaviour with predictable payouts and routing support. The company used a hybrid approach: mid-mile transporters delivered goods to smaller towns, and local riders completed the last-mile deliveries. This model reduced cost without compromising reach.

During these years, India’s logistics landscape split more clearly into two layers. The intercity layer remained dominated by asset-heavy incumbents with predictable line-haul networks. The intra-city layer required adaptability, familiarity, and multi-category throughput, traits that asset-heavy players struggled to replicate. Shadowfax positioned itself squarely in the latter.

Internally, the company began to measure performance with greater precision.

Metrics such as rider productivity, distance per order, zone-level SLA performance, and pickup success rates shaped decisions on allocation and incentives. Enterprise partners appreciated the transparency because it made cost discussions more objective.

Shadowfax’s scale allowed it to raise a $22M Series C, while partnering with Flipkart.

By 2019, the value of multi-category utilisation became obvious. A single-category rider might manage fewer tasks per hour because of idle periods between orders. When riders handled grocery, pharmacy, e-commerce and returns within the same shift, idle time dropped and earnings stabilised. This improved cost competitiveness without requiring aggressive discounting or subsidies.

On the ground, riders experienced the network differently as well.

A grocery drop in the morning, a few pharmacy deliveries in the afternoon and a batch of e-commerce orders in the evening created a predictable workday. For them, Shadowfax was not a category-specific job; it was steady work that responded to real-world demand.

By the end of 2019, the company had evolved into a multi-vertical logistics network with a coherent operating model.

Its economy no longer depended on any single category or city. Instead, utilisation across time, geography and category became the core driver of margins. This was a departure from the Western logic of last-mile delivery, which relied on high-ticket orders, uniform city layouts and consistent demand curves.

India behaved differently, and Shadowfax succeeded because it built around those differences. Yet, as it was finally finding its wings, India was about to be hit with a storm.

Stress Test

When COVID hit in early 2020, India’s logistics sector faced an immediate, unprecedented demand shock.

Grocery and pharmacy orders grew at rates no festive cycle had ever produced. BigBasket, which averaged roughly 150,000 daily orders pre-COVID, publicly disclosed that it handled close to 300,000 orders per day in April 2020.

It also reported an 84% rise in new customers between January and July 2020. In the e-pharmacy segment, several platforms, including 1mg, saw medicine demand rise sharply, with industry estimates suggesting increases of up to 100% in certain metros.

Lockdowns created operational friction almost overnight. With the majority of major Indian cities under strict curfew in April, access restrictions became the biggest bottleneck. Containment zones often barred courier entry, and traditional fixed-route delivery networks saw failure rates climb because their operations depended on predictable access. In several metros, a significant share of pin codes faced restricted delivery windows. Models built on standard routing logic struggled in an environment where regulations could shift multiple times per week.

Shadowfax’s hyperlocal network adapted more quickly because riders were deeply familiar with the neighbourhoods they served.

This local knowledge translated directly into time savings. During the peak of containment restrictions, a rider who knew which gate was open or which lane connected two sealed zones could shorten delivery routes by 15–20 minutes. These micro-advantages compounded across tens of thousands of daily deliveries, helping maintain service reliability during a period when delays were unavoidable.

Consumer behaviour changed sharply as well.

Online grocery adoption surged as first-time users turned to digital channels during lockdown. Order sizes increased as households consolidated purchases into fewer, bulkier baskets. Customers became more flexible with delivery windows, accepting longer fulfilment times, but less tolerant of failed deliveries. A single unsuccessful attempt now carries reputational consequences for merchants and platforms, not just logistical ones, heightening the importance of dependable last-mile execution.

Grocery demand placed unprecedented stress on routing systems. Unlike food delivery, essential baskets were heavier, bulkier and more error-sensitive. BigBasket’s near-doubling of order volume required Shadowfax to adjust its routing logic to account for weight, bag count and customer availability patterns.

In some cities, average travel distance per order rose due to containment rules, requiring constant recalibration of clustering and batching decisions.

Enterprises leaned on networks that could maintain operations despite volatility. BigBasket deepened its engagement with Shadowfax as demand escalated. E-pharmacy players like 1mg relied on flexible last-mile delivery networks to fulfil time-sensitive medicine orders. Swiggy Instamart and Dunzo saw sustained volume spikes. Flipkart’s volumes dipped early in the lockdown but recovered once essential SKUs were permitted again. Meesho’s shipments moved more slowly but remained serviceable even when several logistics partners temporarily paused operations.

Unit economics became more volatile.

Safety equipment, route deviations and frequent checkpoint delays increased the cost per order. Industry estimates suggest a temporary rise of roughly 15–25% in cost-to-serve during the strictest lockdown phases. Despite these pressures, utilisation remained high because multi-category demand filled the day: grocery and pharmacy dominated mornings and afternoons, while e-commerce orders gradually returned to fill the evenings.

This multi-category utilisation helped stabilise margins at a time when pure-play category networks faced steep profitability shocks.

A central structural insight emerged from 2020: logistics models built around rigid optimisation break down when the operating environment changes too quickly. Networks that combined flexible labour, lightweight tech and hyperlocal familiarity adapted better than those that relied solely on automated routing. COVID validated the idea that Indian last-mile delivery is fundamentally a people-centred system, not a purely algorithmic one.

The environment rewarded those who could adjust daily, not those optimised for static conditions.

10 Min Magic

By 2021, Indian logistics entered a phase where every assumption was challenged.

The rise of quick commerce, driven hardest by Blinkit, Instamart and Zepto, compressed consumer expectations faster than any category before it. People who once waited two hours for groceries now expect delivery in under thirty minutes. Consumers reorganised their habits around immediacy.

Dark stores became the nucleus of this change.

Their economics depended less on real estate cost and more on how many orders they could push through each hour. The teams running them understood that every minute of delay multiplied across the day. Store managers often worked with the urgency of a trading desk, watching dashboards, adjusting picker flows, and throttling SKUs when needed. The pressure inside these stores was very different from traditional retail; it demanded speed, discipline and tight coordination.

This environment exposed a new truth: last-mile routing wasn’t about the shortest path anymore. It was now the most important one. A rider who knew which gates were usually locked, which lanes were always free, or which societies allowed direct entry saved precious minutes that algorithms couldn’t anticipate.

When the SLA is 15–30 minutes, those micro-decisions matter as much as macro-optimisation. Riders who had been doing hyperlocal work for years became central to meeting q-commerce expectations; they understood the neighbourhoods intuitively.

Instamart and Blinkit learned quickly that consistency was more valuable than capacity. They needed riders who wouldn't drop off during peak windows. Evening spikes concentrated a disproportionate share of daily orders, and any supply inconsistency caused a visible dip in SLA performance.

Shadowfax’s riders brought predictability. Many treated q-commerce as an anchor shift and supplemented it with pharmacy or e-commerce deliveries, which stabilised their earnings and smoothed the company’s utilisation curve.

India’s structural realities made this model viable in ways outsiders often misunderstand. High urban density meant a dark store could serve thousands of households within a two-kilometre radius. Mixed-use neighbourhoods meant people lived, worked and shopped in overlapping spaces, creating natural order flow. A relatively low cost-to-serve enabled a 15–30-minute delivery at an accessible price point.

Competitors faced different constraints.

Dunzo’s broad concierge model, which once felt like an advantage, became a liability. Riders spent time on non-standard tasks that reduced their per-hour output. When SLAs were compressed, the model struggled with predictability. Delhivery, built around intercity and B2B efficiency, operated on reliability rather than hyperlocal elasticity. It wasn’t a question of capability; it was a structural mismatch.

Q-commerce demanded a network that could stretch and contract with neighbourhood-level volatility.

Inside dark stores, picking and packing became a bottleneck that logistics teams outside the store didn’t always see. While last-mile costs historically dominated fulfilment, the share of picking costs rose materially for high-velocity SKUs. Many stores introduced tighter SKU curation, faster picker training and redesigned floor layouts to shave seconds off each order. It was a silent but critical lever in maintaining SLA targets.

Demand wasn’t uniform across the city. Some clusters saw intense order density, while others remained sporadic. This created operational asymmetry. A rider placed 700 metres off the ideal cluster boundary could miss the entire peak. Q-commerce forced the industry to think at the sub-kilometre level.

Shadowfax’s flexibility made these hyperlocal adjustments easier; riders weren’t locked into a single category or zone. They could rebalance across micro-markets, improving adequate coverage without inflating supply.

By 2022, the operating reality was apparent: q-commerce was a new physics. Every minute mattered. Every metre mattered. Every density node mattered. Networks that adapted to these constraints gained share. Networks designed for more forgiving SLAs faced an uphill battle.

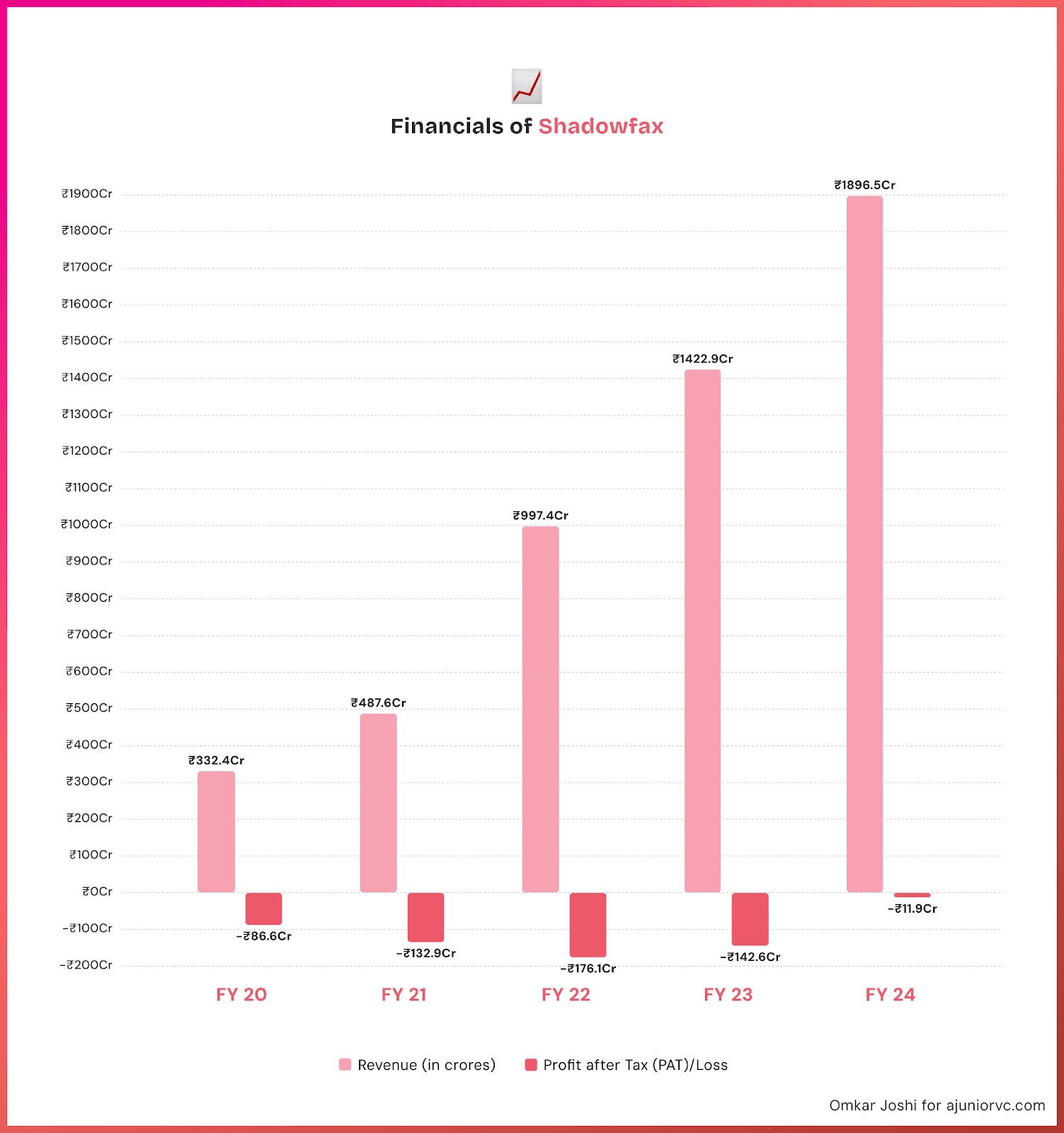

Shadowfax reached 1,400 Cr of revenue and was valued at 3,600 Cr. It was flying like the wind.

Failure Rate

By 2022, Indian e-commerce had entered a phase where optimization at scale was now becoming necessary.

Platforms were no longer fighting only for new customers; they were fighting to reduce leakage, improve reliability and manage the rising complexity of returns. At this stage, logistics networks drifted from pure fulfilment engines into infrastructure partners. For Shadowfax, this was the period when multi-category flexibility turned into enterprise trust.

E-commerce growth slowed compared to the pandemic, but order quality improved. Platforms like Flipkart and Meesho focused on tightening their supply chains: fewer failed deliveries, lower fraud, faster return cycles and more predictable SLAs.

In this environment, last-mile networks with elastic rider pools were better positioned to manage volume volatility. Shadowfax’s network, already accustomed to switching between grocery, q-commerce, pharmacy and e-commerce, handled these fluctuations without the usual margin shocks.

Enterprises valued consistency across weeks, not just peak-day heroics.

Returns emerged as the defining operational challenge. India’s return rate sat around 17–20%, and fashion regularly crossed 30–40%. In smaller cities, return pickups failed 15–18% of the time because people weren’t home or changed their minds.

Reverse logistics in India still cost 2–3 times as much as forward delivery. Sellers felt this in their cash flows every month. In this environment, a logistics network was judged not on how many parcels it delivered, but on how much unpredictability it could absorb.

Enterprises also pushed for deeper visibility.

In earlier years, reporting focused on SLAs, on-time rates and delivery attempts. By 2022–2023, platforms wanted zone-level breakdowns, return attribution, customer unreachability patterns and micro-market behaviour. Shadowfax’s tech stack adapted to this demand.

The company refined its allocation engines to track success probabilities by neighbourhood, time slot and customer type. For enterprise partners, this level of granularity made negotiations more objective. For riders, it meant fewer “dead-end” tasks, orders or returns in zones with low delivery success probabilities.

Tier-2 and tier-3 India grew faster than metros during this period. Shadowfax’s hybrid model, mid-mile aggregation plus hyperlocal last mile, proved more aligned with the economics of small-town India.

Another shift occurred in product mix. Heavy and oversized items, which require specialised handling and different vehicle types, increased as home furnishing and appliance purchases expanded beyond metros. Shadowfax adapted by formalising hybrid fleets, two-wheelers for most items but on-demand access to larger vehicles for select shipments. The ability to switch between vehicle types on short notice added another layer of reliability that enterprises valued.

Competitor behaviour became more pronounced.

Delhivery doubled down on line-haul and B2B strengths. Ecom Express focused on e-commerce reliability and tech-led efficiencies. Dunzo retreated from its broad-service model. Each network leaned deeper into its structural advantages.

By 2023, enterprises treated Shadowfax less as a delivery vendor and more as a “network utility”, a system that absorbed demand across categories, stabilised service levels and managed the growing complexity of customer behaviour.

The company’s role shifted from being a plug-in logistics partner to being an integral layer in the e-commerce operating stack. The company almost reached 2,000 Cr, up 30% from the prior year.

Human Operating System

By 2023, Indian logistics stopped rewarding the loudest scale story and started rewarding the most disciplined one.

E-commerce crossed roughly $60–65B GMV. Tier-2 and Tier-3 India was now nearly 60% of all new e-commerce users, bringing their own behaviour into the mix: more COD, more returns, and very different expectations around timing when last-mile costs make up 50–55% of total fulfilment spend, small acts of flexibility matter. Especially in a country where logistics costs still hover around 13–14% of GDP, much higher than China or the US, any reduction in failed attempts compounds quickly.

The country around Shadowfax was changing, too.

India added over 10,000 km of highways between 2020 and 2023. FASTag reached 98% penetration, cutting road delays by 20–25% on busy corridors. Digitised addresses improved accuracy by 8–12%. These improvements didn’t magically fix logistics, but they created a layer of predictability, something India historically lacked. Predictability enables multi-category networks to become profitable without losing elasticity.

Platforms were also shifting gears. Meesho became India’s highest-volume e-commerce platform with ~2.4 billion annual orders. Its low AOV (₹250–₹350) meant every rupee of cost mattered. Flipkart tightened attribution on failures. Everyone wanted deeper micro-market intelligence—zone-level SLAs, unreachable-customer patterns, time-cluster data. Shadowfax’s system, trained on years of hyperlocal behaviour, was well-suited to this level of detail.

Tier-2 and tier-3 markets became the real growth engine.

COD remained at 45–55%, and customer reliability varied sharply across neighbourhoods. Single-category networks struggled because they were built for predictability. Shadowfax’s riders could drift across categories, matching supply with demand in real time. A rider in Bhilai or Guntur wasn’t thinking in categories; he was thinking in earnings. In solving his own problem, he solved the enterprise’s problem, steady SLAs without expensive overstaffing.

The company crossed 1 billion orders, with a 50% market share in key segments, also becoming profitable.

Shadowfax enters the next decade with this structural advantage. It didn’t build a system that works when everything is perfect. It built a system that works when nothing is. And in India, that’s the more realistic bet.

India’s Logistics Moment Arrives

By 2025, Shadowfax looked less like a young logistics startup and more like a company preparing to operate under public-market scrutiny.

The numbers coming out this year reflected a network that had not only scaled but matured. Shadowfax processed 436 million orders in FY25, growing at a 30% CAGR from FY23 to FY25, a pace few full-stack logistics players have matched in India.

The company now covers nearly 14,758 pin codes, meaning its footprint touches every meaningful consumption pocket in the country.

The push toward profitability also became visible.

In H1 FY26, Shadowfax reported a 114% surge in net profit to ₹21 crore, demonstrating that the economics of elasticity, which many had viewed as risky, were now translating into earnings at scale. This shift didn’t come from dramatic reinvention; it came from the cumulative effect of what the company had built over a decade: multi-category utilisation, human familiarity with micro-markets, and a supply engine that behaves predictably even when demand doesn’t.

Leadership changes added to this maturity arc.

In mid-2025, co-founders Praharsh Chandra and Gaurav Jaithlia were elevated to the Board, signalling a move toward steadier governance as the company prepares for listing. Shadowfax also marked its 10th anniversary, a reminder that the network it operates today was not assembled overnight. Thousands of riders, merchants, partners and micro-markets shaped the company more than strategy documents ever could.

The IPO pursuit, ₹2,000–2,500 crore, depending on market conditions, reflects something larger about India’s logistics moment. Every time a logistics company files for an IPO, it also reflects the state of the economy.

India’s consumption curve is now steep enough, digital infrastructure deep enough, and supply chains formalised enough for logistics networks to be valued as long-term infrastructure, not tactical vendors. The backbone is shifting from jugaad-driven delivery to structured, nationally integrated fulfilment.

Shadowfax sits at an interesting intersection in this shift.

It isn't an asset-heavy line-haul giant like Delhivery, nor is it a captive fleet operator like the q-commerce players. It is a network stitched together by human familiarity and tech-enabled elasticity. These riders know which gates open early, which societies allow direct entry, which micro-markets always need COD, and which lanes can save 4 minutes.

Public markets typically reward predictability, and India’s logistics landscape rarely offers it. Shadowfax’s differentiation is that it has built predictability inside unpredictability.

2025 also marks the first time India’s logistics ecosystem looks collectively investable. FASTag penetration has crossed 98%. Highway expansion has reduced long-haul delays by 20–25%. Digital payments continue to penetrate even COD-heavy regions. Platforms like ONDC are reshaping how demand flows across cities.

The final lens is simple: if the last decade was about scaling e-commerce, the next one is about scaling the infrastructure that makes it reliable. Logistics cannot be robotic in a country where addresses shift, behaviour changes by neighbourhood, and returns run at global highs.

The networks that win will be those that accept India’s complexity, not ignore it. Shadowfax enters the public markets with a model shaped by this complexity, and often strengthened by it.

In replicating a horse faster than the wind, Shadowfax is the dark horse that has become the wind.